Allstate denied my roof claim. You got the letter, and now you’re looking for what works. Allstate has an internal documentation standard their own field adjusters often miss, plus a state complaint record that shows a quarter of denied Allstate cases get paid once the homeowner pushes back. Here’s the playbook, in order.

TL;DR (the seven moves, in order)

- Read the denial letter carefully. “Below your deductible” is a different fight than “no damage.”

- Demand Allstate’s test-square report and confirm they inspected 10 by 10 squares on three or four slopes.

- Document soft-metal hits on vents, gutters, downspouts, drip edge, and AC fins.

- Get two independent roofer inspections using Allstate’s own documentation standard.

- Escalate past the desk adjuster: request a different field adjuster, then the supervisor.

- Invoke the appraisal clause for amount disputes, or hire a bad-faith attorney for coverage denials.

- File a complaint with your state’s Department of Insurance.

Most Allstate denials get reversed between steps 3 and 5 because the original adjuster undershot Allstate’s own standard. The rest reverse at step 7 once a regulator is reading the file.

Why Allstate denies so many hail claims

Denver 7 Investigates pulled open records on Allstate complaints at Colorado’s Division of Insurance. Of 40 closed cases reviewed, 25% resulted in Allstate paying $1,500 to $26,000 after the complaint was filed, even though the Division had no authority to order payment. A Loveland homeowner named Brent described his denial:

They said that they couldn’t see the damage and that the damage didn’t exceed our $2,500 deductible, which is insane.

Brent, Allstate customer, Loveland CO, Denver 7 Investigates on-camera report

A local roofer walked the same barn roof on camera:

From insurance point of view, you’re gonna draw 10 foot box and that box. You want to see 6 to 8 hits. 1, 3, 5, 6, 7, 8. Should this roof be covered? Absolutely.

John Nissen, owner of Roof Link, Berthoud CO, Denver 7 Investigates on-camera report

That roofer logged 21 Allstate claims that year; the first eight were denied. The gap between Allstate’s standard and what field adjusters actually collect is where your appeal lives.

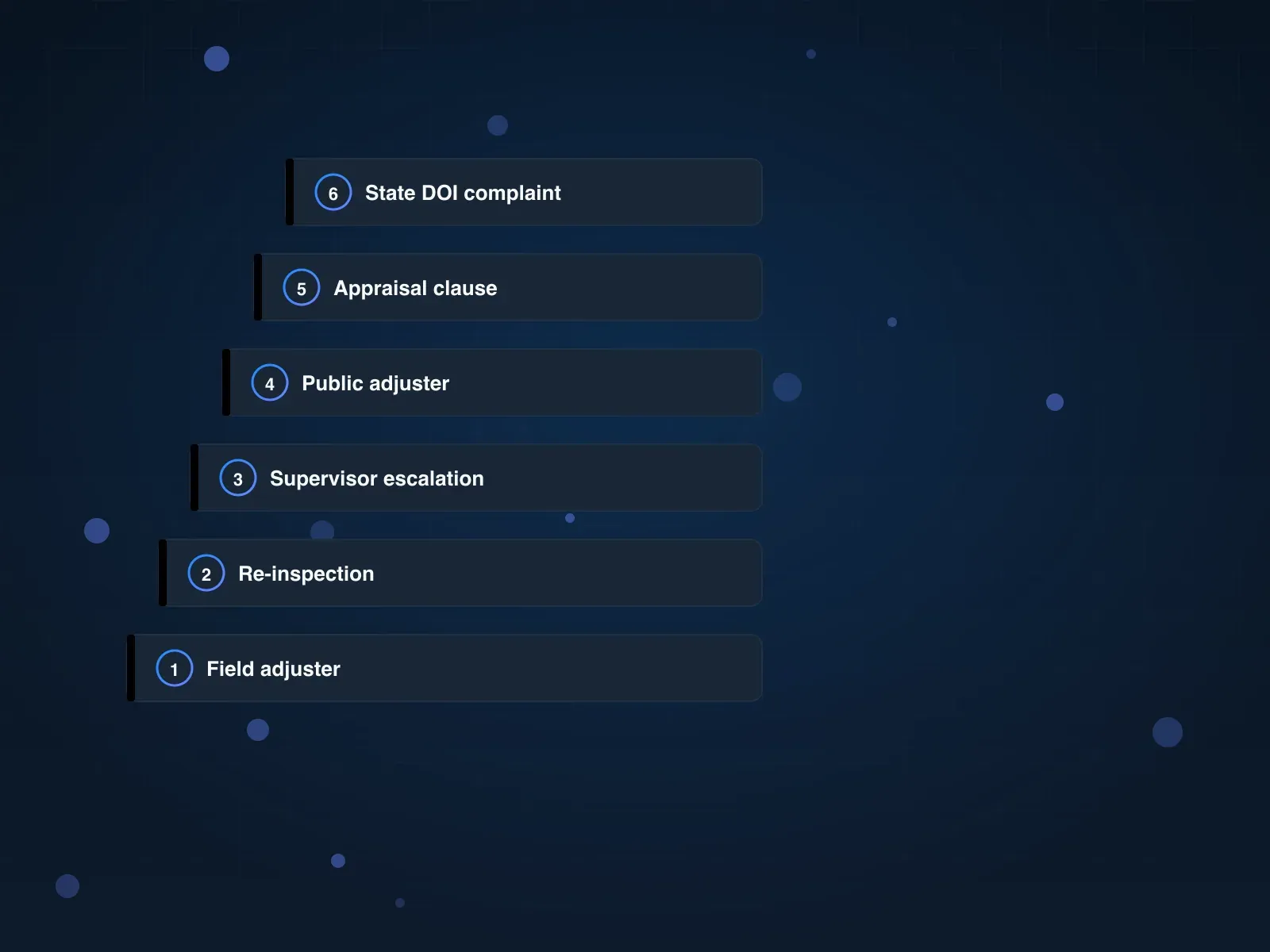

Step 1: Read the denial and identify the exact reason

Allstate denials come in four flavors. Know which one you got before spending a dollar:

- “Below your deductible.” Allstate admits damage; the estimate came in low. Amount dispute. Go to step 2 and dispute the line items.

- “No covered damage.” Coverage denial. Run steps 3–5; attorney at step 6 if Allstate won’t move.

- “Cosmetic damage only.” Impacts admitted, function denied. Pull shingle manufacturer impact spec and document soft metals.

- “Wear and tear” or “age of roof.” Pre-existing or excluded-peril framing. Counter with NOAA hail-size data and neighbor replacements.

If the denial was verbal, email the adjuster: “Are you telling me there’s zero covered hail damage, or that the covered damage is below my deductible?” Get the answer in writing. In neighborhoods where wind/hail deductibles run near $10,000, a “below deductible” denial on a scope Allstate never fully wrote is an amount dispute in disguise, which step 5 unwinds.

Done looks like. Letter in writing, denial category identified, adjuster and supervisor names on file.

Step 2: Demand the test-square report (Allstate’s internal standard)

What to do. Send a written request for the Allstate adjuster’s full inspection record: photos, notes, Xactimate or Symbility estimate with line items, and the test-square documentation. Allstate field adjusters are supposed to chalk a 10 by 10 foot test square on each slope and photograph every hail hit inside it. Most denials that get reversed are reversed because the adjuster skipped this.

An Allstate agent, posting anonymously on r/Insurance, spelled out the internal standard:

I’m an allstate agent. Here is what I see missing from the roofer. I saw 1 pic where a 10x10 are was chalked off. This shows only 1 face of your roof with damage. They will not replace the whole roof with only 1 slope damaged. You need to get the 10x10 samples 3 or 4 slopes showing damage. Also, you can use the soft metal to support hail damage, vents, gutters, trim with damage can also support hail.

u/registeredfake, Allstate agent, r/Insurance thread

A longtime independent adjuster on the same thread added the damage-density threshold:

For Allstate / State Farm to buy a roof, it literally has to have significant hail damage to 75% of the roof.

u/Comfortably_Numm311, 18-year insurance adjuster, r/Insurance thread

Two numbers decide your case: 10x10 squares on three or four slopes, plus enough hits across them to hit the density threshold.

Template: request the claim file. Send by certified mail and email.

Subject: Claim file request, claim [#]

Please send a complete copy of the claim file for claim [#] at [address]: inspection photos, test-square photos and sketches per slope, adjuster notes, the full Symbility or Xactimate estimate with line items, and any cause-of-loss reports. 10 business days.

Policy [#], claim [#]

When it arrives, check: how many test squares and on which slopes; whether they were 10 by 10 (smaller under-counts); whether soft metals were photographed; whether the estimate ran Symbility or Xactimate. Symbility runs about 30% below Xactimate for the same scope in field observation, which is grounds to push back.

Done looks like. Claim file in hand, plus a slope-by-slope list of what the adjuster missed.

Step 3: Document soft-metal damage as corroborating evidence

What to do. Walk the property (or have your roofer walk it) and photograph every piece of soft metal that shows a hail impact. Allstate agents cite soft metals as the tiebreaker on ambiguous shingle cases. If gutters, vents, flashing, drip edge, downspouts, AC fins, and window screens show clean hail impacts, Allstate cannot credibly argue the shingles on the same roof were hit by something else.

An r/Roofing regular described the full list:

soft metal is exactly that kind of stuff, vents, roof jacks, flashing, gutters, downspouts, drip edge, window screens, and even things like the mailbox or AC fins if they got peppered. Those pieces usually show clean hits and it helps support that the storm was real even if the shingle debate turns into a fight.

u/AlonzoFinds, r/Roofing thread

Allstate sometimes denies even with obvious soft-metal damage; one homeowner reported impact marks on every roof jack and solar panel clamp, and Allstate still denied until the homeowner lawyered up. Soft metals alone are often not enough, but soft metals plus test-square documentation plus NOAA data usually are.

How to shoot. Wide shots of each item in context (whole gutter run, whole south side of the AC). Close-ups with a coin for scale. Mailbox, metal lawn furniture, and trash cans if they show matching hits (these prove hail was in your yard). Pull the NOAA Storm Events Database record for your address and staple it to the photos.

Done looks like. A labeled folder with soft-metal photos, a NOAA record, and at least one impact pattern the adjuster did not document.

Step 4: Get two independent roofer inspections

What to do. Hire two local licensed roofers who regularly handle insurance supplements. Each should mark 10 by 10 test squares on three or four slopes, document soft-metal hits, and deliver a written scope plus a counter-estimate in Xactimate-compatible line items. Two roofers’ scopes that match is the evidence step 5 runs on.

How to pick. At least three years in business, a physical local office, a current state license where required, and a current certificate of insurance. Skip door knockers and out-of-state storm chasers (every carrier-side adjuster reads them as a fraud signal). Skip any roofer who offers to “eat” your deductible; that is insurance fraud in most states and sinks the claim. Hire a roofer willing to attend the Allstate re-inspection with you.

The HAAG engineer option. If the case is headed to litigation, a HAAG certified roof inspection runs ~$4,000 and produces an expert-witness report. It’s the right step only after step 6; for most Allstate denials, two licensed local roofers is enough.

Done looks like. Two written scopes with test-square photos on three or four slopes each, matching counts within reason, and a list of the Xactimate line items Allstate left out.

Step 5: Escalate to a supervisor and request a field re-inspection

What to do. The desk adjuster who wrote your denial often never set foot on your roof. Push the file to a field adjuster, then to a supervisor.

The escalation ladder. Desk adjuster → different field adjuster (re-inspection) → desk adjuster’s supervisor → Allstate claims manager → Office of the President (executive complaints line, public at allstate.com) → your state’s DOI (step 7). Climb one rung at a time and document each refusal.

Template: re-inspection and supervisor review. Call, then email:

Subject: Re-inspection and supervisor review request, claim [#]

I am disputing the denial of claim [#] at [address], dated [date]. The original inspection does not meet Allstate’s standard for multi-slope hail damage. Attached: two roofer scopes, test-square photos on [#] slopes, soft-metal photos, and NOAA hail record for [date].

I am requesting (1) a re-inspection by a different field adjuster with my roofer [name, company] on site within 10 business days, and (2) a supervisor review of the original denial, with the supervisor’s name and contact by return email.

Policy [#], claim [#]

Attend the re-inspection. Walk the roof with the new adjuster and your roofer. When the adjuster points at a hit, ask “are you documenting that as hail, on which slope report?” Get answers in writing after.

Timelines. Re-inspection usually schedules in 7 to 14 business days. Most states require a written response to an appeal in 15 to 30 days. Missed deadlines become evidence at step 7.

Done looks like. A new offer, a revised estimate, or a supervisor refusal in writing. Any of the three feeds step 6 or 7.

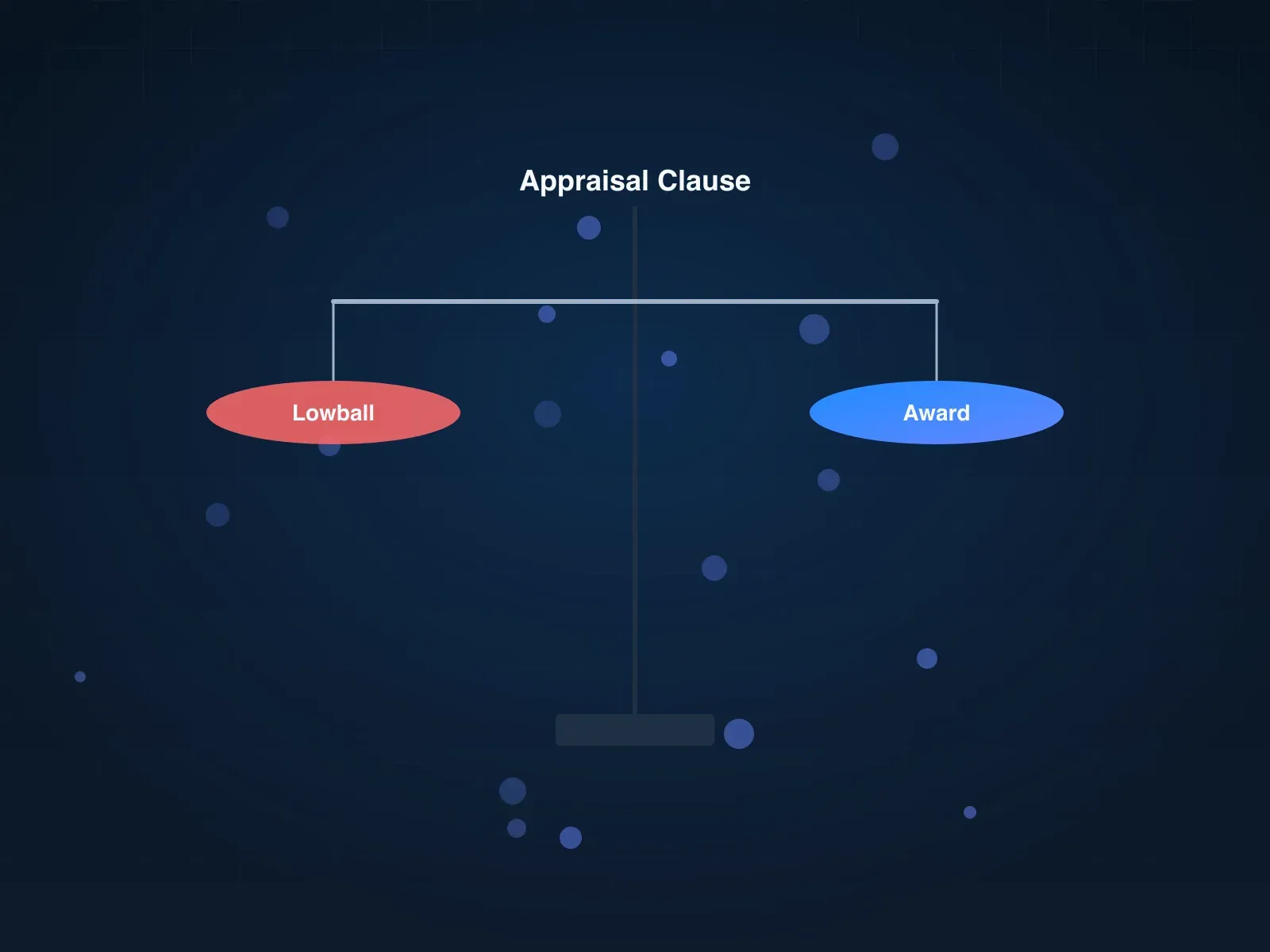

Step 6: Invoke the appraisal clause, or hire a bad-faith attorney

What to do. At this fork, the path splits based on the denial category you identified in step 1.

-

Amount dispute (Allstate admits damage, lowballs the scope): send a written appraisal demand. Each side picks an appraiser, the two pick a neutral umpire, and any two of the three issue a binding award. Appraisal runs $1,000 to $3,000 for your appraiser and resolves in three to six months. See the appraisal clause step-by-step playbook.

-

Coverage denial (Allstate says no covered damage, accuses you of misrepresentation, or missed statutory deadlines): hire a property-damage attorney on contingency. In Colorado, C.R.S. § 10-3-1115 and § 10-3-1116 (2008) allows attorney fees and double damages for unreasonable denial or delay. A Denver bad-faith attorney on camera:

2008 Colorado statute requires insurance companies to not unreasonably deny or delay payment of claims or they’ll pay attorneys fees and double damages.

Brad Levine, Colorado bad-faith attorney, Denver 7 Investigates on-camera report

Florida, Texas, Minnesota, and Washington have parallel statutes. Coverage denials belong with an attorney; appraisal cannot reverse them.

PA vs attorney. PA for amount (10% to 15% contingency). Attorney for coverage denials, delay, or bad faith (30% to 40%, fee-shifting in some states). See the PA vs attorney decision guide for money math.

Done looks like. A signed appraisal award, or a signed attorney engagement with a demand letter to Allstate in the first week.

Step 7: File a state Department of Insurance complaint

What to do. File a formal written complaint with your state’s Department of Insurance (Division, Office, or Commissioner, depending on the state). It is free, fast, and the Denver 7 data shows it works more often than Allstate’s PR line suggests. Colorado’s regulator cannot order payment, yet a quarter of the 40 closed Allstate cases reviewed still paid out $1,500 to $26,000 once the complaint became part of the public record.

What to include. Claim and policy numbers, date of loss, date of denial, the denial reason quoted from Allstate’s letter, dated timeline of every call and email, two roofer scopes with test-square photos, Allstate’s own claim file marked for what the adjuster missed, your re-inspection request plus Allstate’s response, and the NOAA storm record for your date of loss.

Where to file. Colorado: Colorado Division of Insurance. Texas: tdi.texas.gov. Florida: Florida Department of Financial Services. Every state has its own commissioner site, all linked from the National Association of Insurance Commissioners map.

Timelines. Insurer has 15 to 21 days to respond. Investigation runs 4 to 8 weeks on top of that.

Done looks like. A complaint number, Allstate’s written response on regulator letterhead, and in a quarter of Colorado cases, a check before the investigation closes.

Allstate-specific mistakes to avoid

- Do not accept a verbal denial. If the denial came by phone, email the adjuster requesting written confirmation with the policy language cited.

- Do not cash a partial settlement check until you read the release language. Some Allstate checks close the claim when endorsed.

- Do not use Allstate’s preferred contractor without comparing their scope to an independent roofer’s. Preferred contractors often run Symbility pricing that comes in 30% below market.

- Do not sign an AOB contract with any roofer chasing the claim. Allstate has used AOB language against policyholders in Florida and Texas.

- Do not ignore the appeal window. Allstate denial letters give 30 to 180 days. The statute of limitations runs on a separate clock.

For the full escalation decision tree (PA at what dollar range, attorney at what denial type, DOI timing), see the master pillar playbook. Allstate short version: supervisor at step 5, appraisal or attorney at step 6, DOI at step 7.

Key takeaways

- Your Allstate denial is not final. A quarter of Colorado DOI complaints against Allstate paid $1,500 to $26,000 after the complaint.

- Allstate’s internal standard is 10 by 10 test squares on three or four slopes. Many denials fail that standard.

- Soft-metal damage on vents, gutters, drip edge, and AC fins is the tiebreaker on ambiguous shingle cases.

- The desk adjuster often never climbed the roof. Request a field re-inspection with a different adjuster.

- Appraisal reverses amount disputes; attorneys reverse coverage denials. Know the fight before you hire.

- Colorado C.R.S. § 10-3-1115 and 1116 allow attorney fees and double damages for unreasonable denial. Florida, Texas, Minnesota, and Washington have parallel statutes.

- File the DOI complaint if a supervisor says no. It is free and works.

FAQ

How do I dispute an Allstate roof claim denial?

Request the written denial citing specific policy language, demand the adjuster’s full claim file, and document 10 by 10 test squares on three or four slopes plus soft-metal damage. Request a re-inspection by a different field adjuster and escalate to a supervisor. If Allstate still refuses, invoke appraisal for amount disputes, hire a bad-faith attorney for coverage denials, and file a state DOI complaint.

What is the Allstate 10x10 test square rule?

Allstate’s internal documentation standard, confirmed by an Allstate agent on r/Insurance, is a 10 by 10 foot chalked test square on each slope with every hail impact photographed. Adjusters are supposed to document three or four slopes before approving a full replacement. Many denials happen because the adjuster only documented one slope, which fails the standard.

What is the Allstate 75% roof damage rule?

An 18-year adjuster on r/Insurance described the Allstate and State Farm internal threshold as “significant hail damage to 75% of the roof” before full replacement. This is not a published policy number; it is the operational threshold adjusters work from. Counter with test squares across all four slopes plus soft-metal damage.

How do I escalate an Allstate roof claim after a supervisor denial?

File a complaint with your state’s Department of Insurance (free, 4 to 8 weeks) and consult a property-damage attorney experienced with bad-faith litigation. Colorado, Texas, Florida, Minnesota, and Washington have statutes that allow fee-shifting or double damages. Denver 7 Investigates found 25% of reviewed Colorado Allstate complaints paid $1,500 to $26,000 after filing.

Can I sue Allstate for denying my roof claim?

Yes. An attorney can sue Allstate for breach of contract, and in several states for bad faith (fee-shifting plus extra-contractual damages). Colorado C.R.S. § 10-3-1115 and 1116 allows attorney fees and double damages for unreasonable denial or delay. Most attorneys take these on contingency; cases run 9 to 24 months.

Why does Allstate use Symbility instead of Xactimate?

Some Allstate claims estimate in Symbility, which field observation in hail-belt states puts at about 30% below Xactimate for the same scope. That pricing gap is one of the strongest arguments at appraisal: your independent appraiser can insist on Xactimate or local-market comparables, and the umpire is supposed to decide on market pricing, not carrier software.

How long do I have to appeal an Allstate roof claim denial?

Most Allstate denial letters give 30 to 180 days to file a formal appeal. The statute of limitations for a lawsuit is typically 1 to 5 years from the date of loss (Florida: 2 years for hurricane or windstorm, 5 years for other perils). Mark both on the calendar the day the denial arrives; they run independently.

Does filing an Allstate hail claim raise my home insurance rates?

Filing does not raise your rate during the current policy period, but it can raise your renewal premium or cause non-renewal if you filed multiple claims in the past three to five years. Every claim, paid or denied, shows up on your CLUE report. A single weather claim rarely triggers non-renewal alone.

What if Allstate says my hail damage is cosmetic only?

Cosmetic exclusions vary by policy and state. Pull your shingle manufacturer’s impact spec (GAF, Owens Corning, and CertainTeed publish 1.25 to 2-inch thresholds that void warranty when struck) and pair it with NOAA hail-size data. Add soft-metal damage photos. Minnesota and Iowa “matching” case law sometimes forces full replacement even on damage otherwise classified as cosmetic.

Should I hire a public adjuster or an attorney for an Allstate denial?

PA for amount disputes (10% to 15% contingency); attorney for coverage denials or missed deadlines (30% to 40%, fee-shifting in some states). PAs handle scope and line-item fights; attorneys handle breach of contract and bad faith. Many cases use both: PA through appraisal, attorney if Allstate refuses to pay the award.

What if Allstate’s preferred contractor is lowballing the scope?

You are not required to use Allstate’s preferred contractor in any state. Preferred contractors often have per-claim pricing agreements that favor the carrier. Hire your own local licensed roofer, get a scope in Xactimate line items, and attach the preferred contractor’s scope to your dispute as comparison evidence.

Related reading

- hail damage insurance claim denial playbook (master hub)

- how to invoke the appraisal clause

- public adjuster vs attorney

- Xactimate estimate gap audit

- hail under 1 inch doesn’t damage shingles

- CLUE report and non-renewal risk

- hail damage evidence checklist

- how to hire an honest roofer

Running this playbook against Allstate? Generate a free Allstate-ready evidence pack with NOAA hail data, a 10x10 test-square checklist, and the supervisor-escalation email template.