State Farm denied my roof claim. If that sentence describes your afternoon, the next paragraph should help. A State Farm roof claim has its own rules, threshold, and timing levers. The 25-year insurance restoration specialist with a 95% approval rate walks every State Farm adjuster meeting with chalk in his hand. You can run a version of the same playbook.

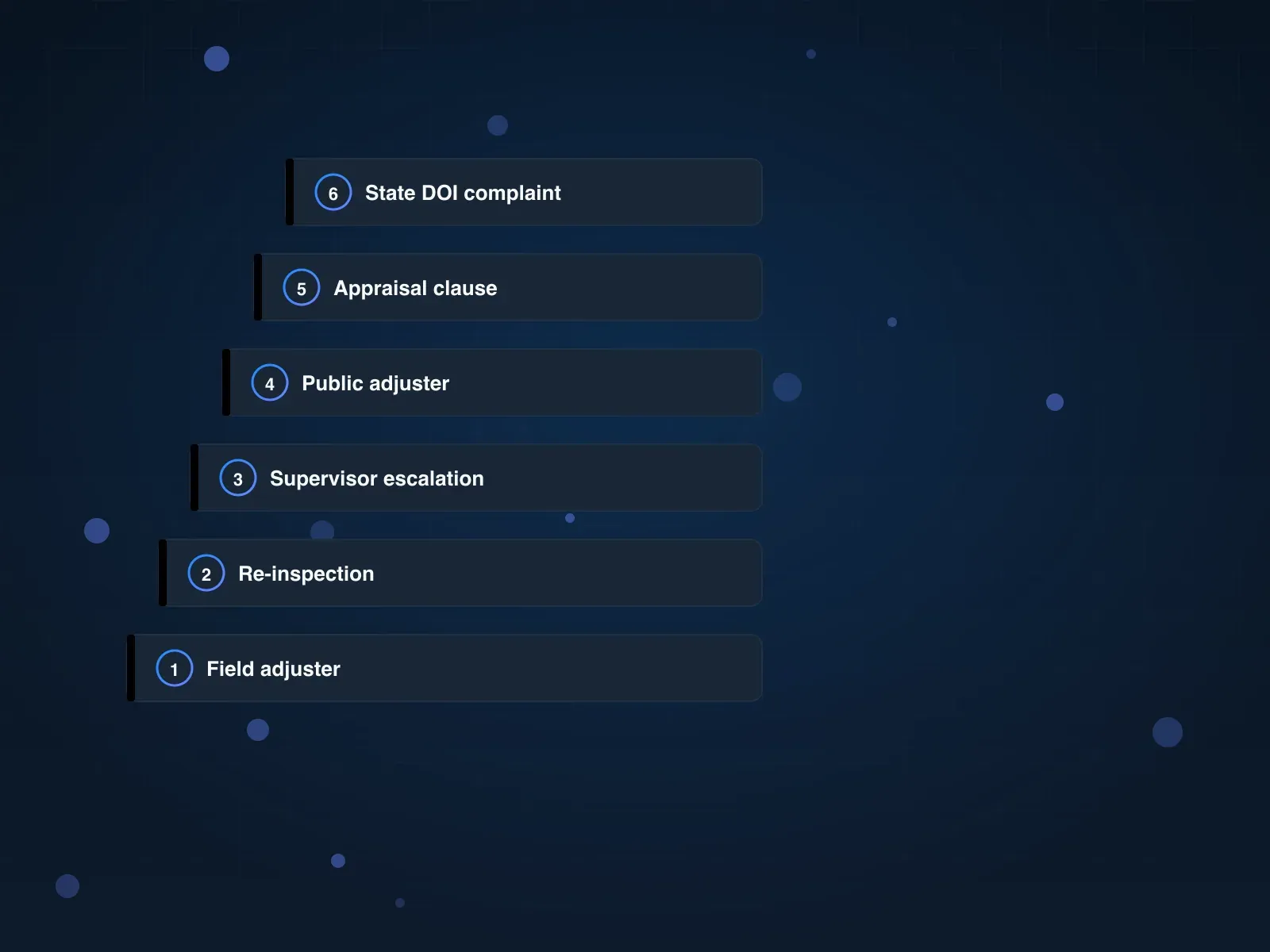

TL;DR (the four moves State Farm responds to)

- Document damage before you file. State Farm looks for 4 to 5 real hail hits per 10 by 10 test square plus soft-metal corroboration.

- Get a Xactimate estimate from your own roofer before accepting State Farm’s scope. Ridge, starter, waste factor, and overhead are the line items State Farm most often cuts.

- Understand the 3-claim non-renewal math. In Illinois and Indiana, State Farm has dropped homeowners after three hail claims in three years.

- If State Farm still underpays after a re-inspection, invoke the appraisal clause. State Farm allows 2 years from date of loss (longer than most carriers) to get this in motion.

If you are on claim one and pre-filing, step 3 is actually step 1. If you are post-denial, run 1, 2, 4 in order.

Why State Farm denies so many hail claims

State Farm led Illinois home-insurance complaints with 1,224 filings at the state DOI since January 2022, roughly 2.4x the Allstate count (515), per ABC7 Chicago I-Team’s public data review. State Farm’s statement to the I-Team emphasized volume, not approval rate: “Year to date, we have received over 83,000 catastrophe claims excluding auto, and we have paid out over $800 million in these two states alone.”

A denied Chicago homeowner on the same broadcast:

We did the cars, we did an umbrella policy, we did the house, everything. And to them, just look at us and go, nope, no way. It’s very disheartening.

Homeowner on-camera, ABC7 Chicago I-Team report

The pattern is not universal. A State Farm customer on r/Insurance reported two hail-replacements in thirteen years with zero friction:

My roof has been replaced twice by State Farm in 13 years due to hail… I have had zero issues with State Farm they have always covered me with no problems.

u/[deleted], r/Insurance thread

Both true. The approved claim had clean documentation, a direct State Farm adjuster inspection, and a roof age that matched the storm date. The denied ones usually do not.

Step 1: Document damage before filing (State Farm’s 4 to 5 hits per 10 by 10 standard)

What State Farm is looking for. Chad Michael, a 25-year insurance restoration specialist who runs State Farm claims for a living, spelled the carrier’s internal threshold on camera:

Actually State Farm is not as stringent because they only need four to five hits in a 10 x 10 area but they need to actually be hail hits, okay.

Chad Michael, 25-year insurance restoration specialist, How to Get a State Farm Roof Claim Approved

That is looser than Allstate’s 6 to 8 hits (see the Allstate denied my roof claim playbook), but the “actually be hail hits” half is the trap. State Farm adjusters know blistering, nail pops, thermal cracking, and mechanical damage when they see it. Chad’s line in the sand:

That’s a blister. So talk to me about a blister, what is that? Where the Sun beats on that and it basically pops, so you see any embedded granules in there? All you see is the fibers. You see the fibers inside there, that’s not hail. You showing an adjuster that as hail, he’s going to tell you to get bent.

Chad Michael, How to Get a State Farm Roof Claim Approved

“Get bent” is the moment the meeting ends in a denial. Do not walk an adjuster onto a roof with anything you cannot confidently call hail.

The chalk-marking walkthrough. Before the adjuster arrives, walk the roof with your roofer and mark every real hail hit with a short chalk line (not a circle). On the walk-through, lead the adjuster to each mark and ask, one at a time, “do you agree this is hail, or disagree?” Verbatim from Chad:

When I meet that adjuster I always ask them, do you agree or disagree this is hail after I marked it. If they disagree then I ask them why. If they agree then I say great, we’ve got other ones in the 10 foot by 10 foot area. How many do you need in a 10 by 10 foot area? And you stay calm and cordial. Eventually once you get that chalk in their hand and they start circling, game over.

Chad Michael, How to Get a State Farm Roof Claim Approved

The moment the adjuster takes the chalk and circles hits themselves, the claim shifts from “prove it” to “document it.”

Start with soft metals, not shingles. Take the adjuster to the soft-metal damage first: gutters, vents, drip edge, downspouts, AC condenser fins, window screens, ridge caps. This is where State Farm adjusters form their impression that hail was in the yard. After that, the shingle call becomes “is this hail” instead of “was there even a storm.”

What to photograph. Wide shots of each soft-metal item in context, close-ups with a coin for scale, and the test square on three or four slopes with every hit numbered. Pull the NOAA Storm Events Database record for your date of loss and staple it to the folder.

Done looks like. A labeled folder with test-square photos, soft-metal photos, and a NOAA record, handed to the adjuster before they climb the ladder.

Step 2: Get a Xactimate estimate from your own roofer first

Why set the anchor. State Farm writes estimates in Xactimate, the same pricing software your roofer uses. Both sides pull from the same database, but State Farm’s scope often leaves out the line items that matter most. Chad on what adjusters resist:

Adjusters also don’t like to pay for ridge and starter a lot of time, and also pay for too little of amount, too low of an amount for the waste factor.

Chad Michael, How to Get a State Farm Roof Claim Approved

Waste factor on a gable roof often runs 18%; State Farm’s default is near 5%. On a $25,000 scope that is $3,000 to $4,000 on a single line. A complete roofer Xactimate estimate with 18% waste, ridge-and-starter line items, detach-and-reset on soft metals, and overhead-and-profit broken out puts you arguing specific numbers instead of abstract fairness.

The 2010 overhead-and-profit change. State Farm moved its O&P approval standard from “three or more trades” (clear objective rule) to “reaches a level of complexity and coordination” (subjective, carrier decides). Most hail roof projects qualify if you document the trades list (roofing, gutter, sheet metal, painting, insulation) and the coordination between them. Put it on paper.

Accept the first check, then supplement. Chad’s counter to State Farm’s predictable lowball opener:

Go ahead and send the money. Send that money. And I would say to the contractor, go over, pick up the money and start lining up the repairs, but at the same time initiating a round of supplementing. How many rounds of supplementing can you do? The answer: as many times as necessary.

Chad Michael, How to Get a State Farm Roof Claim Approved

State Farm opens low (a $30,000 offer on a $40,000 scope is typical), then pays more in supplements once demolition uncovers rotten decking, step flashing, code-upgraded ice-and-water shield, and vent replacements. Your roofer files supplements as items surface. Homeowner ends up at full scope with no contentious meetings.

Done looks like. Your roofer’s complete Xactimate scope delivered before the re-inspection, plus a supplement plan for every line the first estimate omitted. The Xactimate estimate gap audit guide walks the audit.

Step 3: Understand the non-renewal risk math before you file

The three-claim rule. The most-cited line on r/Insurance about State Farm non-renewal:

You’ve already filed 2 claims. If you file a 3rd, you are almost guaranteed to be non-renewed.

u/FindTheOthers623, r/Insurance thread

Community heuristic, not published policy. The ABC7 Chicago case of Jen and Phil Hibbard (Crown Point, IN) put numbers on it: three hail events in a single year, a roofer estimate around $23,000, State Farm denied the claims then dropped the family after three hail claims in three years (total count over a nineteen-year relationship). The wife on camera:

State Farm was choosing not to renew our homeowner’s policy because we’ve made too many claims. And it was very devastating.

Jen Hibbard, State Farm customer, ABC7 Chicago I-Team report

What the timing looks like. State Farm cannot cancel mid-term without cause. They can non-renew at your renewal date with 60 days of written notice (Illinois and Indiana both run 60-day notice). Every claim, paid or denied or cancelled, shows up on your CLUE report for five to seven years. The CLUE report and non-renewal risk guide covers the pre-file math.

When not to file. If the scope is under $5,000 and your deductible is $2,500 or more, the math almost never works. You pay half, spend a claim slot State Farm will remember, and push your CLUE report toward non-renewal. Fix it out of pocket and preserve the clean record.

Counter-evidence. The same Reddit thread includes a State Farm customer with two paid hail replacements in thirteen years and no non-renewal. Both that homeowner’s claims followed a State Farm adjuster inspection, a clean Xactimate scope, and a storm date lined up with NOAA data. Documentation quality is the single biggest variable inside your control.

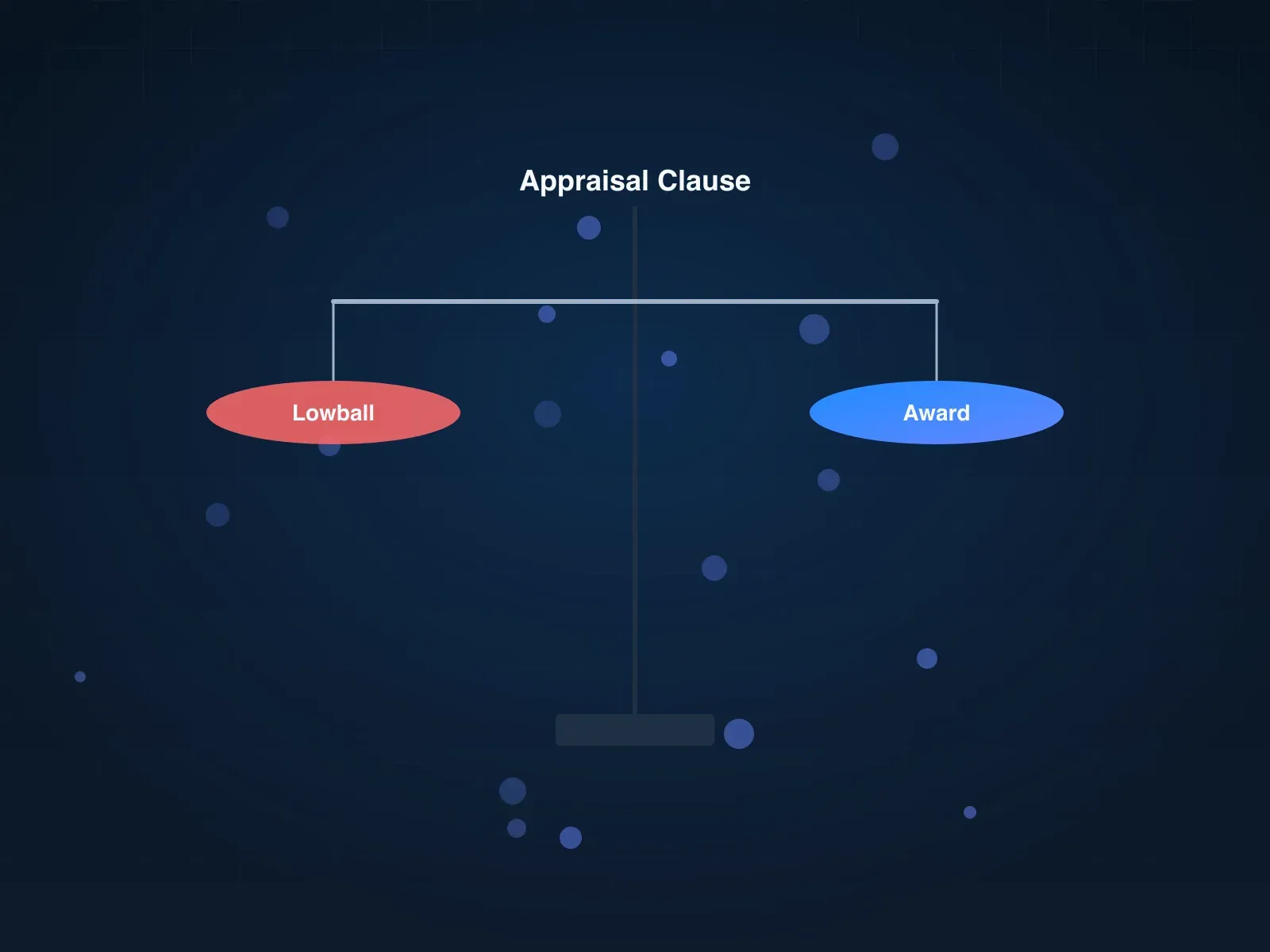

Step 4: Invoke the appraisal clause if State Farm still underpays

Appraisal is your lever on amount disputes. Every standard State Farm homeowner policy includes an appraisal clause. If State Farm admits damage but disputes the amount, demand appraisal in writing: each side picks an appraiser, the two pick a neutral umpire, any two of the three issue a binding award.

A real State Farm appraisal reversal. A 2021 Denver State Farm claim (documented by Metro City Roofing) shows how it plays out. The first adjuster was on the roof under 60 seconds before denying shingle damage as “not hail.” On re-inspection, the second adjuster denied shingles again but marked 19 roof vents as hail damage plus hits on gutters, downspouts, window screens, and garage doors. With soft-metal admissions on the record and half the neighborhood already replaced, the homeowner sent an Appraisal Demand Letter. The two appraisers met, agreed the roof had extensive hail damage, and the full replacement was approved.

Template: Appraisal Demand Letter.

Subject: Appraisal demand, claim [#], policy [#]

Pursuant to the appraisal provision of my State Farm homeowner policy, I am invoking appraisal as to the amount of loss for claim [#] at [address]. My appraiser is [name, address, phone, credentials]. Please provide your appraiser’s name and contact within 20 days of this letter so the two can select a neutral umpire. The award will be binding as to the amount of loss.

Policy [#], claim [#]

Send certified mail with return receipt.

Timing: State Farm’s 2-year window. State Farm is one of the few carriers that allows two years from date of loss to file, versus one year for most. The appraisal window is longer, but so is State Farm’s patience for dragging a claim out. Plan three to six months from demand to signed award.

Budget and who to hire. Your appraiser runs $1,000 to $3,000 flat. Hire a licensed public adjuster, a retired carrier field adjuster, or a Xactimate-certified contractor with appraisal experience. Do not hire your own roofer; appraisers are supposed to be impartial, and State Farm will challenge a roofer-appraiser on that ground. The step-by-step appraisal clause playbook covers the mechanics.

Done looks like. A signed award, and a State Farm check for award minus deductible. Most State Farm appraisals settle at the two-appraiser stage without the umpire.

Common State Farm denial phrases and the counter for each

- “Blistering, not hail.” Pull your roofer’s close-up photos showing the embedded granules and mat bruising; blisters look like popped fiber exposure without granule embedment.

- “Nail pops, not hail.” Chad’s rule: if there is a nail visible in the hit, it is mechanical. Do not bring those to the meeting.

- “Damage does not exceed your deductible.” Demand the full Xactimate line items and compare to your roofer’s scope. This is a step-2 fight, not a step-4 fight.

- “Mechanical damage.” The carrier is blaming foot traffic, installation, or prior maintenance. Your roofer’s install compliance statement and original storm date are the counter.

- “Filed past the two-year window.” Confirm your exact date of loss against the NOAA record and your filing date. State Farm’s 2-year clock starts on the storm date, not the notice date.

For generic denial phrases across all carriers (wear and tear, pre-existing, cosmetic only, wind-driven rain), see the master pillar playbook.

State Farm-specific mistakes to avoid

-

Do not hear about your claim from your roofer. If a contractor is telling you what State Farm said before State Farm has contacted you directly, that is a fraud-pattern signal:

Where were you in this process and why did you hear this from your “friend” instead of State Farm? Did a State Farm adjuster not come out at all? This sounds like potential fraud.

u/theladyoctane, r/Insurance thread

-

Do not file a marginal third claim. Two paid claims in the last three to five years plus a third triggers near-automatic non-renewal. Pay a sub-$5,000 repair out of pocket.

-

Do not accept the first State Farm offer as final. Multi-round supplementation is how full approvals happen.

-

Do not argue with the adjuster on the roof. Run the chalk-marking agree-or-disagree tour instead. Contentious meetings end in denial.

-

Do not present blistering or nail pops as hail. You will be told to get bent, and the rest of the claim pays the price.

When to escalate: the decision tree

Work top to bottom. Stop at the first row that matches your State Farm situation.

| Your situation | Best next step |

|---|---|

| State Farm admits damage, disputes amount. Dispute under $10K | Supplement rounds through your roofer, no PA needed |

| Amount dispute, $10K to $75K, single peril | Appraisal clause (step 4 above) |

| Amount dispute, $75K+, or multiple perils (hail + wind + water) | Hire a public adjuster (10% to 15% contingency) |

| State Farm denies coverage outright (“not a covered loss”) | Property-damage attorney; appraisal will not apply |

| Supervisor denied the re-inspection appeal | Illinois/state DOI complaint + appraisal demand, simultaneously |

| State Farm missed the 2-year or state statutory response window | DOI complaint + bad-faith attorney consult |

| State Farm accused you of misrepresentation or late notice | Attorney immediately. Do not speak to the adjuster without counsel |

| Claim drags past 12 months with no resolution | DOI complaint + bad-faith attorney, simultaneously |

Most State Farm homeowners resolve at step 2 (roofer Xactimate + supplementation) or step 4 (appraisal). DOI complaints and attorneys are the lever when the carrier is stalling past statutory timelines.

Key takeaways

- State Farm needs 4 to 5 real hail hits per 10 by 10 test square, plus soft-metal corroboration.

- Chad Michael’s chalk-marking “agree or disagree” walkthrough flips an adjuster meeting from adversarial to collaborative. Start on the soft metals.

- Get your roofer’s full Xactimate before State Farm writes theirs. Ridge, starter, 18% waste factor, and O&P are the line items most often cut.

- Accept State Farm’s first check and supplement repeatedly. That is how they pay in full.

- The 3-claim rule is real. State Farm led Illinois complaints with 1,224 filings since 2022; three claims in three to five years triggers non-renewal at your next renewal.

- State Farm allows 2 years from date of loss, longer than most. The appraisal clause reverses amount disputes within that window.

FAQ

How do I dispute a State Farm roof claim denial?

Request the denial in writing with the specific policy language cited, demand the full adjuster file including the Xactimate estimate, and document 10 by 10 test squares on three or four slopes with 4 to 5 hail hits each plus soft-metal damage. Request a re-inspection with a different adjuster and your roofer on site. If State Farm still underpays, invoke the appraisal clause or file a state DOI complaint.

What is the State Farm 3-claim non-renewal rule?

State Farm does not publish a hard rule, but a third claim in a rolling three-to-five-year window near-guarantees non-renewal at your next renewal date. ABC7 Chicago documented State Farm dropping the Hibbard family after three hail claims in three years. Every claim, paid or denied, shows up on your CLUE report for five to seven years.

Does State Farm require 10x10 test squares for hail damage?

Yes. A 25-year insurance restoration specialist working State Farm claims put the internal threshold at 4 to 5 real hail hits per 10 by 10 test square. That is looser than Allstate’s 6 to 8, but State Farm denies on blistering, nail pops, and mechanical damage passed off as hail. Document three or four slopes plus soft metals.

How long do I have to file a State Farm hail claim?

State Farm allows two years from date of loss, longer than the one-year window most carriers use. The statute of limitations on a lawsuit runs on a separate clock (typically 1 to 5 years, depending on state and peril). Mark both on the calendar the day the storm hits.

Can I sue State Farm for denying my roof claim?

Yes. An attorney can sue State Farm for breach of contract, and in Colorado, Florida, Texas, Minnesota, and Washington for bad faith (unreasonable denial or delay). Most take these on contingency (30% to 40%, fee-shifting in some states). Typical timeline 9 to 24 months.

Will State Farm drop me after a roof claim?

State Farm cannot cancel mid-term without cause. They can non-renew at renewal with 60 days of written notice (exact window varies by state). A single weather claim rarely triggers non-renewal; two or three paid claims in the last three to five years move you into the non-renewal pool even if the claims were legitimate.

How do I invoke the appraisal clause on a State Farm claim?

Send a written Appraisal Demand Letter by certified mail citing the appraisal provision. State Farm names an appraiser within 20 days; the two jointly select a neutral umpire; any two of the three issue a binding award on amount. Budget $1,000 to $3,000 for your appraiser and three to six months to resolution.

What is a State Farm Xactimate estimate?

Xactimate is the pricing software State Farm writes most roof estimates in. Line items State Farm commonly cuts: ridge and starter courses, waste factor (default near 5%, actual often 18%), detach-and-reset on soft metals, and O&P (State Farm’s 2010 rule change replaced “3 or more trades” with a subjective “complexity and coordination” standard).

How do I escalate a State Farm roof claim after a supervisor denial?

File a complaint with your state’s Department of Insurance (free, 4 to 8 weeks) and consult a bad-faith attorney in parallel. Illinois received over 3,000 home insurance complaints since January 2022; State Farm led with 1,224. The Illinois DOI gives the insurer 21 days to respond, then runs a 4 to 6 week investigation.

Why did State Farm deny my hail damage claim?

The five most-common denial reasons: “damage below the deductible” (amount dispute disguised), “blistering not hail” (shingle-aging call), “mechanical damage” (blame the roofer or prior owner), “filed past the 2-year window,” and “pre-existing damage.” Each has a specific counter; see the denial-phrases section above.

Will State Farm raise my rates after a hail claim?

Filing does not raise your rate during the current policy term. State Farm can raise your renewal premium, and state rate filings in Illinois and elsewhere have pushed premiums 10% to 20% year over year independent of individual claims. Every paid or denied claim appears on your CLUE report for every future carrier to see.

Related reading

- hail damage insurance claim denial playbook (master hub)

- Allstate denied my roof claim

- how to invoke the appraisal clause

- Xactimate estimate gap audit

- CLUE report and non-renewal risk

- public adjuster vs attorney

- hail damage evidence checklist

Running the State Farm playbook on a fresh denial? Generate a free State Farm-ready evidence pack: NOAA hail data for your address, the 4-to-5-hit 10 by 10 checklist, and the agree-or-disagree walkthrough script. 2 minutes.