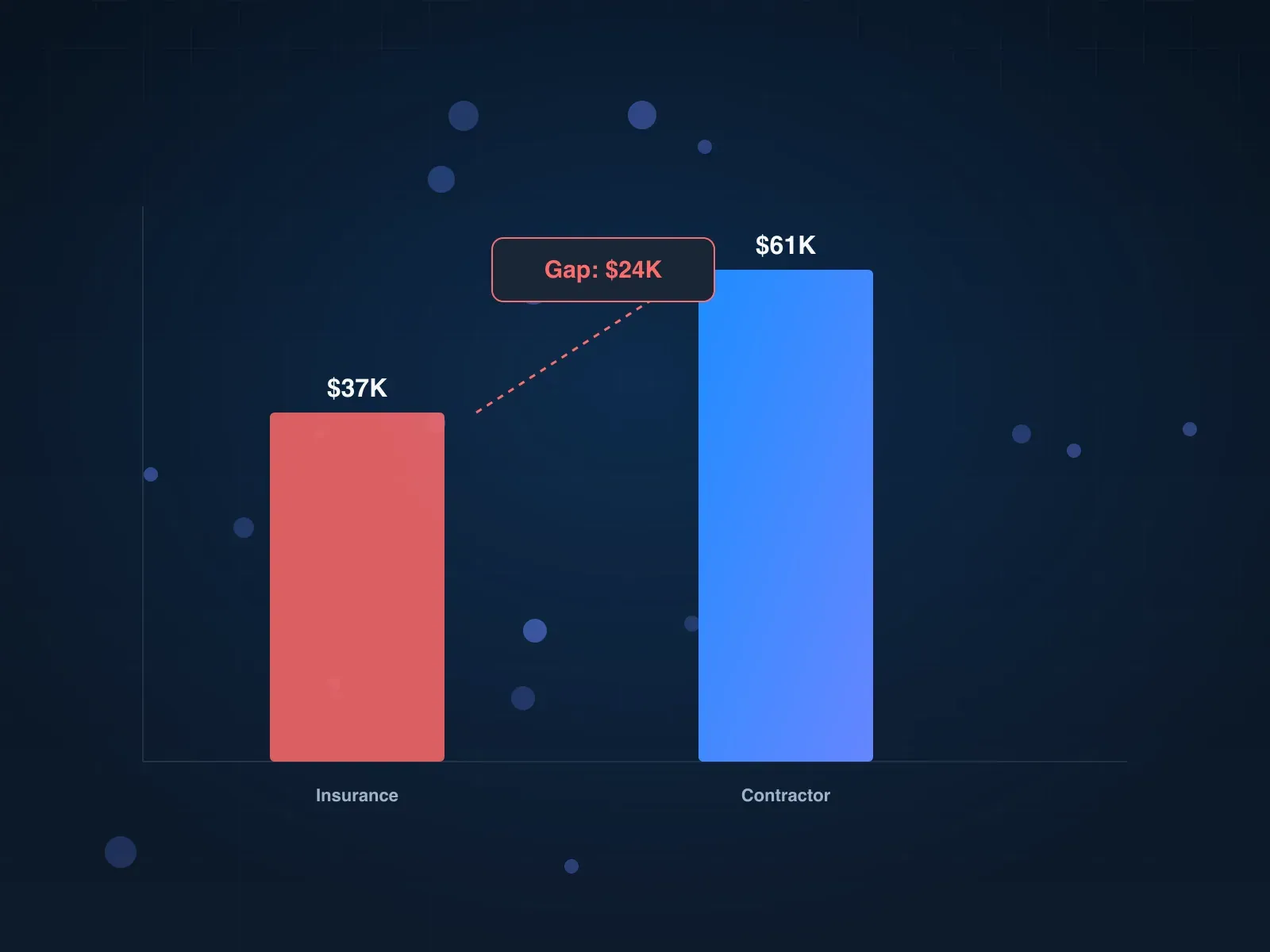

Same Xactimate software, two different numbers. An r/HomeInspections homeowner posted that his insurance estimate came in at $37K; his roofer, using the same Xactimate, came back at $61K. The carrier paid the roofer’s number. The $24K gap wasn’t about whether the roof was damaged. It was about line items the carrier’s estimate left out: soft metals, drip edge, IWS, ridge cap, detach-and-reset, code upgrades, and O&P. Here’s how to read the estimate, spot the omissions, and file the supplemental.

TL;DR (the four moves, in order)

- Read the carrier’s Xactimate estimate front to back. Note the price list code, every line item, depreciation column, and whether O&P is included.

- Mark the omissions: soft metals, code upgrades, detach-and-reset, interior damage, ridge and starter, drip edge, IWS, and O&P.

- Have your roofer write a counter-estimate in the same software on current price list, with photos linked to every line.

- File a supplemental claim with the line-item diff. Send the re-inspection request in the same envelope, 14-day window.

Plan 30 to 90 days from supplemental to second check. If the carrier refuses or returns the same number, invoke the appraisal clause and run that clock in parallel.

Why the gap exists in the first place

Xactimate isn’t a price list. It’s a database of construction line items (codes, labor units, material costs) that both carriers and contractors use to write the same estimate in the same format. The reason two estimates come back $24K apart is that the carrier’s adjuster picks a smaller scope, uses a lower-paying price list (Symbility instead of Xactimate, or an outdated month), denies overhead and profit by default, leaves out covered items (soft metals, code upgrades, detach-and-reset), and applies depreciation aggressively on the first ACV payment.

Each of those is a separate fight. The gap is the sum of all of them. A homeowner who closed the gap by walking the carrier through the missing items:

Insurance gave me a $37K price. Roofing company came back at $61K. Insurance and roofing companies use the same estimation software. Insurance left a lot of things out. Roofing Co. was thorough. Insurance had no choice but to honor the Roofing Cos. estimate.

u/mrkprsn, r/HomeInspections thread

The carrier did not argue the line items were wrong. They were forced to honor a complete scope once it was on paper.

The rest of this guide is the audit process that turns the left bar into the right bar.

Step 1: Read the carrier’s Xactimate estimate front to back

The carrier’s Xactimate estimate is a 15 to 60 page PDF sent after inspection. The middle pages are the line-item scope (the part that matters). Find these five things:

- Price list code. Top of the line-item section, looks like

MNXX8X_OCT26orTXMC8X_NOV26. The first letters are state and metro; the last 5 characters are the price list month. If the date is older than 90 days, demand a refresh on the supplemental. - Software. Top of the document: “Xactimate,” “Symbility,” or “Verisk Estimating.” Per Metro City Roofing, Symbility prices approximately 30% below Xactimate on the same scope. If the carrier wrote in Symbility, the entire scope is under-market by ~30%. That’s its own line in your gap diff.

- Line items. Each line is a code (

RFG SHL,RFG IWS,GTR ALUM 6"), a quantity, a unit (SQ for squares, LF for linear feet, EA for each), a unit price, and a total. Read every line. Anything missing will not be paid. - O&P. Search for “overhead” or “O&P.” If zero or absent, the carrier denied it. That’s a 20% line on the entire scope.

- Depreciation. A column on the right of each line item, as dollars and a percentage. On a 10-year-old 30-year shingle, expect ~33% off the total. If your policy is RCV (Replacement Cost Value), the depreciation is held back and paid as a second check after you complete the work. If your policy is ACV (Actual Cash Value), the depreciation is gone. Confirm which you have on the declarations page before any other math.

Done looks like. A printed estimate with the price list, software, every missing or zero-quantity line, the O&P line (or its absence), and the depreciation column highlighted. You’re ready to mark omissions.

Step 2: Mark the line items the carrier left out

Five categories show up in almost every underpaid claim. Walk each one against your printed estimate and flag what’s missing or under-quantity.

Soft metals (the most common omission)

Soft metals are the thin metal pieces on the roof and house: vents, pipe boots, drip edge, step flashing, gutters, downspouts, screens, AC condenser fins. Hail dents them visibly, and the dents are impossible to argue. A r/homeowners post made the dollar impact concrete: the carrier initially offered roughly the cost of a single bundle of shingles before a public adjuster expanded scope to include gutters and screens, moving the final settlement to $52K on a $1K deductible (u/BAHGate, r/homeowners thread).

Counter-move. Photograph every soft-metal piece with a coin or chalk for scale, add a line per item on the supplemental. Check your policy first for soft-metal exclusions; some lower-tier policies exclude “metal pieces of the roof” (gutters and downspouts included).

Code upgrades (the second-most-common)

When you replace a roof, current building code triggers may apply: drip edge on rakes and eaves, ice and water shield at the eave and around penetrations, solid decking under older spaced sheathing, Class 4 shingles in some hail-prone municipalities. If your policy includes “ordinance or law” or “code coverage” (most do), the carrier owes those upgrades. Minnesota’s 2024 Campbell decision confirmed insurers must cover code-required upgrades integral to the repair; other states have similar precedent.

Counter-move. Pull the local building code for the specific items and add a line for each that’s missing, with the building code section number.

Detach-and-reset (anything attached to the roof)

If your roof has a satellite dish, solar array, gutter guards, HVAC condenser, or lightning rod, those items must be detached, the new roof installed under them, and then reset. Detach-and-reset is a separate Xactimate line per item, and carriers leave it out routinely. On a roof with solar, the missing line can be $3,000 to $10,000.

Counter-move. Walk the roof, one photo per attached item, add a detach-and-reset line per item. If solar is involved, get the solar installer to write a separate proposal; the carrier shouldn’t be writing solar work itself.

Overhead and profit (O&P)

O&P is the 10% + 10% margin (20% total) a general contractor adds when coordinating multiple trades. State Farm changed the automatic trigger to a vague “complexity and coordination” test in the early 2010s; other carriers followed. So O&P is now denied by default. The argument: complexity is met whenever three or more trades are involved, a permit is pulled, or the roof has solar/satellite/HVAC requiring sequenced trades.

Counter-move. Add the O&P line (10% + 10% on full scope). In the letter, list every trade (roofing, gutters, painting, HVAC reset, solar reset, interior repair) and cite “complexity and coordination.” Carriers often quietly add O&P back once it’s called out by name.

Interior damage

Hail through a roof can soak insulation and stain drywall ceilings. If the carrier never went into the attic, interior damage isn’t on the estimate. It’s a covered loss under dwelling coverage, separate from roof line items.

Counter-move. Photograph the attic and any ceiling staining. Get a drywall and insulation estimate. Add the lines to the supplemental.

Step 3: Have your roofer write the counter-estimate

The counter-estimate isn’t a quote on letterhead. It’s a complete Xactimate document in the same software the carrier used, with every line item, photos linked, and the same price list code. If the counter isn’t in Xactimate, it doesn’t count.

Who can write it. A Xactimate-licensed contractor, a licensed public adjuster, or a retired carrier field adjuster.

What the counter-estimate must include. Current month’s price list; every soft-metal item, ridge and starter, drip edge, IWS, code upgrade, and detach-and-reset with quantities matched to the roof; O&P at 10% + 10% on full scope with the trade list; photos linked to every disputed line; a cover page with the carrier’s number, your number, and the gap.

What it costs. Most roofers write it free as part of winning the job. A public adjuster writes it for 10% to 15% of recovery. A consulting estimator runs $500 to $1,500 flat. Start with the roofer.

Contractor agreement red flag. Don’t sign a “whatever insurance pays” contract. Use exclusivity in exchange for a complete Xactimate scope with matching photos.

Done looks like. A printed Xactimate counter-estimate, the gap diff, and a one-page cover letter.

Step 4: File the supplemental claim with the gap evidence

The supplemental is a written request to revise the estimate based on omitted scope. It’s not a re-inspection, and it’s not an appraisal demand. It’s the first lever to pull.

The supplemental letter template.

Subject: Supplemental claim, claim [#], policy [#]

I am submitting a supplemental claim for additional scope on [property address]. The original estimate dated [DATE] was written for $[X]; my contractor’s complete Xactimate estimate, attached, is $[Y]. The $[Y-X] gap is the sum of:

- Soft metals: gutters ([LF]), downspouts ([EA]), drip edge ([LF]), AC fins, screens. See photos 1 to [N].

- Code upgrades per [code section]: IWS at penetrations and eaves ([SF]), solid decking ([SF]), Class 4 shingles per [ordinance].

- Detach-and-reset: [items].

- O&P at 10% + 10%, trades involved: [list].

- Price list refresh from [carrier’s code] to current [code/date].

I am also requesting re-inspection by a different field adjuster within 14 days. If the re-inspection produces an acceptable revised offer, no further action is needed. Otherwise, please proceed with the supplemental review against the attached Xactimate document. Please confirm receipt within 5 business days.

[Name, date, policy and claim numbers] Sent via certified mail, return receipt [#]

How to send it. Certified mail with return receipt to the claim handler, plus email the same day. Save both receipts.

Response window. Most carriers respond within 14 to 30 days with either a revised estimate or a written denial of specific line items. If the window passes without acknowledgment, send a follow-up letter citing the missed deadline and copy your state DOI.

What carriers do at this point. One of three things: (1) quietly add some or all of the missing line items and issue a revised estimate plus a second check (about half the time on a well-documented supplemental); (2) agree to a re-inspection and come back with a revised number (plan 14 to 45 days); or (3) refuse the supplemental in writing, item by item, which triggers the appraisal clause.

The supplemental doesn’t waive your other rights. Accepting the initial check (or any partial payment) doesn’t stop you from coming back for the gap. Most policies and most state statutes explicitly preserve your right to a supplemental for additional or omitted scope discovered during repairs.

Done looks like. Certified receipt in your file, carrier’s written acknowledgment, and either a revised estimate or a written denial naming the rejected line items.

What not to do

- Don’t sign a “whatever insurance pays” contract. That makes the roofer indifferent to your gap. Use exclusivity in exchange for a full Xactimate scope.

- Don’t let the roofer “eat your deductible.” Illegal in most states (insurance fraud), and it tells you they’ll inflate the scope, which gets the supplemental denied.

- Don’t pay the contractor in full from the first check. RCV policies pay in two checks. Paying everything up front leaves nothing to bridge the 30-to-90-day second-check gap.

- Don’t accept a verbal “we’ll take care of the gap.” Get the revised estimate in writing. The carrier can email a revised PDF same-day.

- Don’t skip the re-inspection request. Even if you invoked appraisal, run the re-inspection in parallel; the carrier sometimes resolves the gap there and saves you the appraisal cost.

- Don’t send a “quote” instead of an Xactimate counter-estimate. Letterhead quotes don’t translate into the carrier’s system.

When to escalate (decision tree)

| Your situation | Best next step | Timeline | Cost |

|---|---|---|---|

| Carrier open to revising, gap any size | Re-inspection request (same letter, 14-day window) | 2 to 6 weeks | $0 |

| Carrier refuses supplemental in writing, gap over $5K | Invoke the appraisal clause | 3 to 6 months | $1,750 to $5,500 |

| Gap over $15K, don’t want to manage the fight | Public adjuster on contingency (10% to 15%) | 2 to 6 months | 10 to 15% of recovery |

| Carrier acted in bad faith (silent past windows, lost photos, repeated denials) | Property-damage attorney on contingency | 9 to 24 months | 30 to 40% (fee-shifting in some states) |

| Carrier missed statutory response windows | State DOI complaint | 4 to 8 weeks | $0 |

Run re-inspection and appraisal in parallel. The calendar will beat you if you wait for one to fail before starting the next.

Key takeaways

- The gap is the sum of five carrier choices: smaller scope, Symbility (~30% under Xactimate), denied O&P, omitted soft metals and code upgrades, aggressive depreciation.

- Find the price list code, software, line items, O&P line, and depreciation column on the carrier’s estimate first.

- Have your roofer write the counter-estimate in the same software, current month’s price list, photos linked to every disputed line.

- File the supplemental with a 14-day re-inspection request in the same envelope. Certified mail plus email, same day.

- Add O&P at 10% + 10% on full scope and list every trade. Carriers often add it back once called out by name.

- Plan 30 to 90 days from supplemental to second check. If the carrier refuses, invoke the appraisal clause in parallel.

FAQ

What is an Xactimate estimate?

An Xactimate estimate is a structured cost document written in Xactimate (made by Verisk), the industry-standard pricing platform for property claims. It lists every line item by code, quantity, unit price, total, depreciation, and O&P. Both carriers and contractors use the same software, so the gap between carrier and roofer estimates comes from scope and price list choices, not the tool.

What does an Xactimate estimate sample look like?

A typical sample is a 15 to 60 page PDF: claim summary on page 1, scope by building section in the middle, and a price list reference at the back. The price list code at the top of the scope (like MNXX8X_OCT26) tells you which metro and month the rates come from. Ask your roofer for a redacted sample if you haven’t seen one.

How do I read Xactimate line items?

Each line is a code, quantity, unit, unit price, total, and depreciation. Codes follow a category prefix: RFG for roofing, GTR for gutters, DRY for drywall. The unit is SQ for squares (100 sq ft of roofing), LF for linear feet, EA for each, SF for square feet. Read every line; anything missing will not be paid.

What is O&P (overhead and profit) on an Xactimate estimate?

O&P is a 20% margin (10% overhead plus 10% profit) added when a general contractor coordinates multiple trades. Until the early 2010s, O&P triggered automatically on three-trade jobs; carriers changed the standard to a vague “complexity and coordination” test. To get O&P now, list every trade and cite the standard in the supplemental.

What is detach-and-reset on an Xactimate estimate?

Detach-and-reset is a separate line item for any object attached to the roof that has to be removed during replacement and reinstalled: satellite dish, solar panels, gutter guards, lightning rod, roof-mounted HVAC. Each item is its own line. Carriers leave these out routinely. Walk the roof, photograph each item, and add a line per item to the supplemental.

Why is my roofer’s Xactimate estimate higher than insurance?

Five reasons, usually all at once: the carrier wrote in Symbility (~30% under Xactimate), denied O&P, omitted soft metals, omitted code upgrades (IWS, drip edge, Class 4 shingles), and left out detach-and-reset on attached items. The gap is the sum of those omissions. A line-item diff turns it into a supplemental claim.

How do I file a supplemental insurance claim?

Send a written supplemental letter to the claim handler with three attachments: your roofer’s complete Xactimate counter-estimate, photos linked to every disputed line, and a one-page diff. Send certified mail with return receipt plus email the same day. Most carriers respond within 14 to 30 days with a revised estimate or a written denial.

What is the Xactimate vs Symbility pricing difference?

Symbility (now part of CoreLogic) typically prices the same scope about 30% below Xactimate in the same metro. Allstate, Safeco, and Liberty Mutual moved to Symbility to lower payouts. Demand a re-write in Xactimate on the supplemental, or take the gap to appraisal.

What if insurance underpaid my roof claim?

File a supplemental with a complete Xactimate counter-estimate from your roofer. If the carrier denies or returns the same number, request a re-inspection, then invoke appraisal if that doesn’t close the gap. A PA on contingency is the option if you don’t want to manage the fight yourself.

How long does a supplemental claim take?

Plan 30 to 90 days from supplemental request to second check on a clean case. The carrier has 14 to 30 days to acknowledge and respond. Re-inspection adds 2 to 6 weeks; appraisal adds 3 to 6 months. Past 90 days with no carrier response, file a state DOI complaint citing the missed window.

Can I file a supplemental claim after I already cashed the first check?

Yes. Cashing the first check isn’t a release. Most policies and state statutes preserve your right to a supplemental for additional or omitted scope discovered during repairs. If the carrier asks you to sign a release in exchange for the first check, don’t sign it.

Related reading

- hail damage insurance claim denial playbook (master hub)

- Allstate denied my roof claim

- State Farm roof claim denial guide

- hail under 1 inch denial dispute

- invoke the appraisal clause

- public adjuster vs attorney

- hail damage evidence checklist

Ready to file the supplemental? Generate a supplemental-ready line-item diff from your carrier’s Xactimate PDF and your roofer’s counter-estimate. Lists omissions by category and pre-fills the supplemental letter with your claim number.