You opened the letter. Your hail damage insurance claim got denied, or the check came in so low it covers a box of shingles, not a roof. You are not out of options. About 37% of U.S. property insurance claims got denied or underpaid in 2024, and hail is the biggest line item inside that number. This is the source-backed playbook, in the order a working public adjuster would run it.

TL;DR (do these seven things, in order)

- Get the denial in writing, with the specific policy language they relied on.

- Request the adjuster’s full claim file: photos, notes, Xactimate estimate.

- Get two independent local roofer inspections, with 10 by 10 test squares on three or four slopes.

- File a written re-inspection request and have your roofer present for it.

- If the carrier admits damage but lowballs the amount, invoke the appraisal clause.

- If the carrier denies coverage outright or drags past statutory deadlines, hire a public adjuster or a property-damage attorney.

- File a complaint with your state Department of Insurance once the carrier refuses to move.

Stop at any step that resolves the claim. Most homeowners never get past step three because no one told them steps four through seven existed.

Why this is happening to you

Your first clue is usually the inspection itself. One homeowner on r/Roofing put it plainly:

the inspection felt kind of quick, like he looked around, took photos, tapped a few spots, then left.

u/Own_Lion2788, r/Roofing thread

There is a reason for that. A Colorado contractor on camera explained that a field adjuster usually gets paid around $250 per inspection with a target of 10 inspections a day. A denial takes ten minutes. A full approval takes forty to sixty minutes of report-writing afterward. The pay structure rewards fast denials, so that is what you got. A documented State Farm case from Denver went further: the adjuster was on the roof for under 60 seconds before deciding it wasn’t hail. That same case got reversed at appraisal, with a full roof replacement approved.

The denial letter is the starting line, not the end. Every step below is a lever the policy and your state law already hand you. You just have to pull them in order.

Step 1: Save the denial letter and get it in writing

What to do. Make sure you have a written denial letter that states the specific reason and cites the exact policy language the carrier is relying on. If you only got a phone call, call back and email the adjuster asking for a written denial. Save every email, letter, and voicemail in a single folder labeled with your claim number.

How to do it. Send a short email to the adjuster, copying their supervisor if you have the name:

Subject: Written denial requested, claim [#]

Per our call on [date], please send me a written denial letter for claim [#] stating the specific reason for denial and the policy section you are relying on. Please also confirm the date you issued the denial and the appeal window under my policy.

Print the denial letter and the email. Scan them back in as a PDF. This is your evidence baseline.

What to look for in the letter. Carriers deny hail claims using a small set of stock phrases. Know which one you got, because the counter-move is different for each:

- Damage does not exceed your deductible. The carrier admits damage, disputes amount. This is the one appraisal is built for.

- Cosmetic only or cosmetic damage exclusion. The carrier admits impacts exist but says they do not affect function.

- Wear and tear or age of roof. The carrier is blaming time, not the storm.

- Pre-existing damage. The carrier says the damage was there before the policy started, or before the storm date you cited.

- Hail under one inch does not damage shingles. A rule of thumb, not a spec. Your shingle manufacturer’s published impact threshold will usually contradict it.

What it costs, how long. $0, about 15 minutes once the letter arrives. Your appeal window usually runs 60 to 180 days from the denial date, with 30 to 60 days typical under most standard homeowner policies. Do not let it start counting down without you.

Done looks like. You have the denial letter in hand, you know the exact reason cited, and you have saved it plus every email in one folder. You are ready for step two.

Step 2: Request the adjuster’s full claim file

What to do. Send a written request for the adjuster’s complete claim file: their photos, their inspection notes, their Xactimate estimate with line items, and any engineering reports or sketches. You have a statutory right to this in almost every state.

How to do it. Send this by certified mail with return receipt, plus email for a paper trail:

Subject: Claim file request, claim [#]

Please send me a complete copy of the claim file for claim [#], including all inspection photos, the adjuster’s notes, the full Xactimate or Symbility estimate with line items, any engineering or cause-of-loss reports, and all internal correspondence related to the denial. I request this within 10 business days per [state] insurance regulations.

Policy [#] [Your name, address, phone]

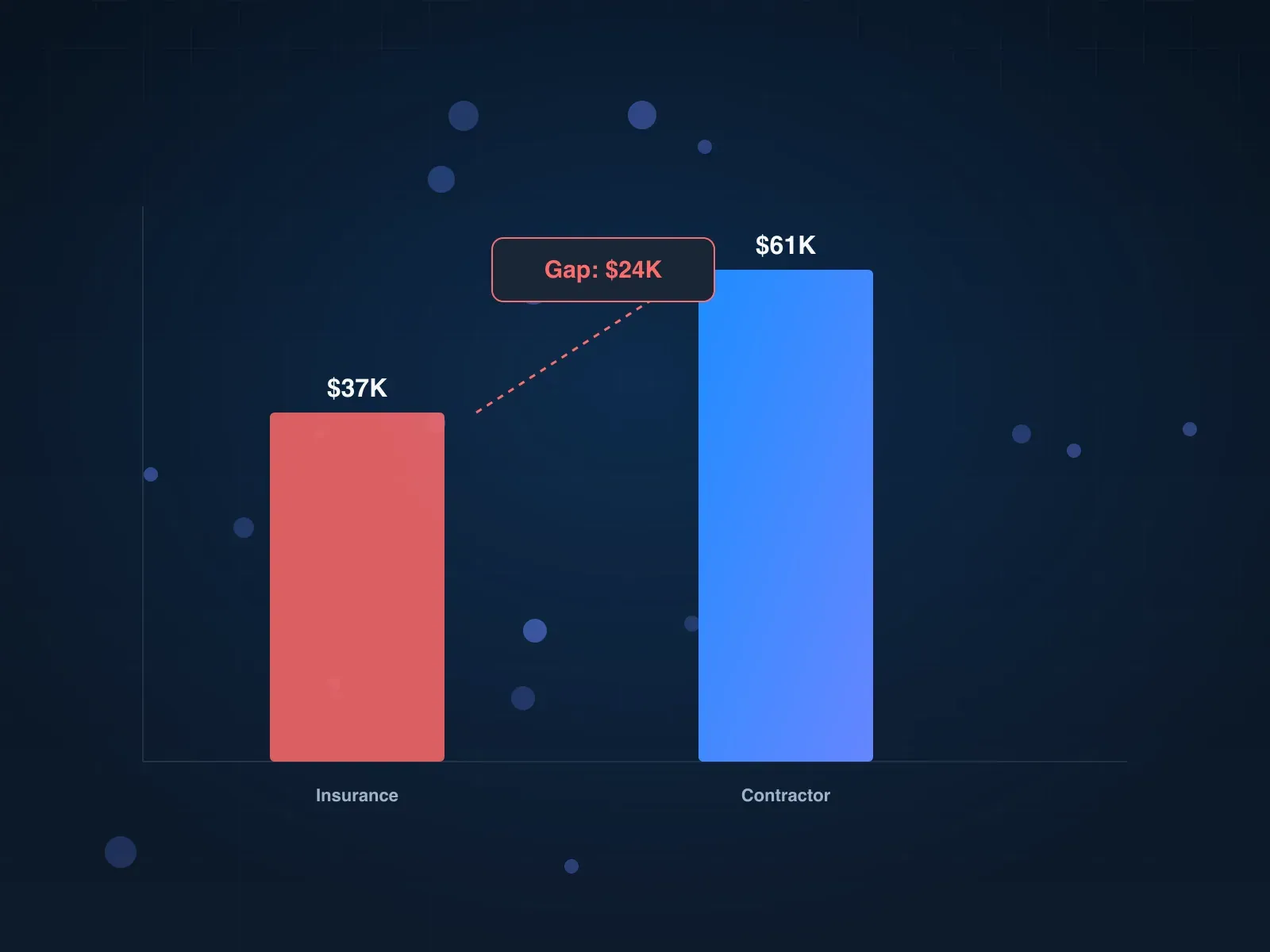

What to compare when it arrives. Put the adjuster’s photos side by side with the photos your roofer took. Count the test squares the adjuster marked and on how many roof slopes. Look at the Xactimate line items and note what is missing: soft metals (vents, gutters, drip edge, downspouts, AC fins), interior water stains, code-required upgrades, detach-and-reset line items, overhead and profit. Real-world gaps between the adjuster’s Xactimate estimate and a local roofer’s Xactimate estimate often run 30% to 65% using the same software. One homeowner on r/HomeInspections summarized it:

Insurance gave me a $37K price. Roofing company came back at $61K. Insurance and roofing companies use the same estimation software. Insurance left a lot of things out. Roofing Co. was thorough. Insurance had no choice but to honor the Roofing Cos. estimate.

u/mrkprsn, r/HomeInspections thread

What it costs, how long. $0 for the request, $10 to $20 if they charge a copy fee. Most carriers deliver the file in 5 to 15 business days. If they miss that window, that is itself a data point for a later state complaint.

Done looks like. You have the adjuster’s photos, notes, and line-item estimate in front of you, and you have a list of at least three categories the estimate left out.

Step 3: Get two independent roofer inspections

What to do. Hire two local, licensed roofers who regularly handle insurance supplements. You want a written scope of damage and a counter-estimate in Xactimate or Xactimate-compatible line items. One roofer’s opinion is an opinion. Two that agree is evidence.

How to vet them. Use this short list before you let anyone on your roof:

-

At least three years in business, with a physical local office.

-

A state license on the official state licensing site, if your state requires one, plus a current certificate of insurance (general liability and workers’ comp).

-

Ten or more reviews on Google, with a look at the one-star reviews to see how they handle problems.

-

A flat refusal to pay or promise to “eat” your deductible. That offer is a federal-level insurance fraud issue in most states and will tank your claim if the carrier finds out.

-

No door-knocker out-of-state storm chasers. One commenter summarized the community view:

Red flags are out of state companies and door knockers. Never go with a national company unless they have a legitimate office in your area. A lot of times they send 10 salesmen out to a storm area and leave once the work dries up.

u/GayNotGayTony, r/Roofing thread

What the roofer should actually document. A 10 by 10 foot test square chalked off on each of three or four roof slopes, with every hail hit circled, plus close-ups with a coin or ruler for scale. An Allstate agent on r/Insurance laid out what carriers inside the building look for:

I’m an allstate agent. Here is what I see missing from the roofer. I saw 1 pic where a 10x10 are was chalked off. This shows only 1 face of your roof with damage. They will not replace the whole roof with only 1 slope damaged. You need to get the 10x10 samples 3 or 4 slopes showing damage. Also, you can use the soft metal to support hail damage, vents, gutters, trim with damage can also support hail.

u/registeredfake, r/Insurance thread

Another r/Insurance commenter with 18 years of adjusting experience was blunt about the Allstate and State Farm internal threshold:

For Allstate / State Farm to buy a roof, it literally has to have significant hail damage to 75% of the roof.

u/Comfortably_Numm311, r/Insurance thread

That is why a single-slope set of photos almost always loses. Three or four slopes is the floor, not the ceiling.

Soft metals are the tiebreaker. If the adjuster says the shingles are ambiguous, the dents and bruises on gutters, downspouts, vents, flashing, ridge caps, and AC condenser fins often settle the argument. An r/Roofing regular put it well:

soft metal is exactly that kind of stuff, vents, roof jacks, flashing, gutters, downspouts, drip edge, window screens, and even things like the mailbox or AC fins if they got peppered. Those pieces usually show clean hits and it helps support that the storm was real even if the shingle debate turns into a fight.

u/AlonzoFinds, r/Roofing thread

What it costs, how long. Inspections are typically free from a local roofer who wants the job. Allow 5 to 10 days to schedule and deliver written estimates. If you want an independent expert witness who can testify later, a HAAG-certified inspection runs about $4,000 out of pocket, which is worth it only for a large claim headed to litigation.

Done looks like. Two written estimates, each with photos of test squares on three or four slopes, soft-metal damage documentation, and a Xactimate or Xactimate-compatible line-item list that matches the damage.

Step 4: File a written re-inspection request, with your roofer present

What to do. Write to the carrier and ask for a second inspection, by a different adjuster, with your roofer on site at the same time. You are not asking for permission. You are telling them what you need.

How to do it. Call the adjuster, then follow with this email so it is in writing. The veteran advice from r/Roofing:

I would start by calling the adjuster and then follow up by email so it is all in writing. You do not need to come in hot, just say you are concerned the scope may be incomplete because the inspection was quick, and you want a reinspection after you gathered more documentation.

u/AlonzoFinds, r/Roofing thread

A template you can adapt:

Subject: Re-inspection request, claim [#]

I am requesting a re-inspection of claim [#] at [address], with a different adjuster and with my roofer [name, company] present. The original inspection on [date] ran approximately [minutes] and the resulting estimate omitted [list the 3 to 5 biggest missing items]. I have attached photos of test squares on [#] slopes, soft-metal damage, and a written scope from [roofer]. Please confirm a re-inspection date within 10 business days.

Policy [#], Claim [#] [Name, phone]

Attend the inspection. Be there. Do not leave your roofer alone with the adjuster, and do not leave the adjuster alone. Walk the roof with both of them. Ask the adjuster to mark what they see on each slope with chalk. When they point at a spot, ask, “is that hail or is that blistering, and what are you writing in the report?” Get the answers on email after.

Why this works. A second pair of eyes, under watchful supervision, finds what the first one missed. A Denver contractor describing a State Farm re-inspection:

We started finding hail damage and finding enough to Warrant a total loss Insurance claim for this roof.

Roofing contractor, on-camera narration in Why Was This Roof Insurance Claim Denied… Then APPROVED?

What it costs, how long. $0. The carrier usually schedules within 7 to 14 business days. If they refuse, note the refusal in writing. It strengthens the Department of Insurance complaint at step 7.

Done looks like. You have a second written inspection report from the carrier. Either the carrier reverses itself now, or you have two conflicting reports from the same insurer, which is the evidence you need for step 5.

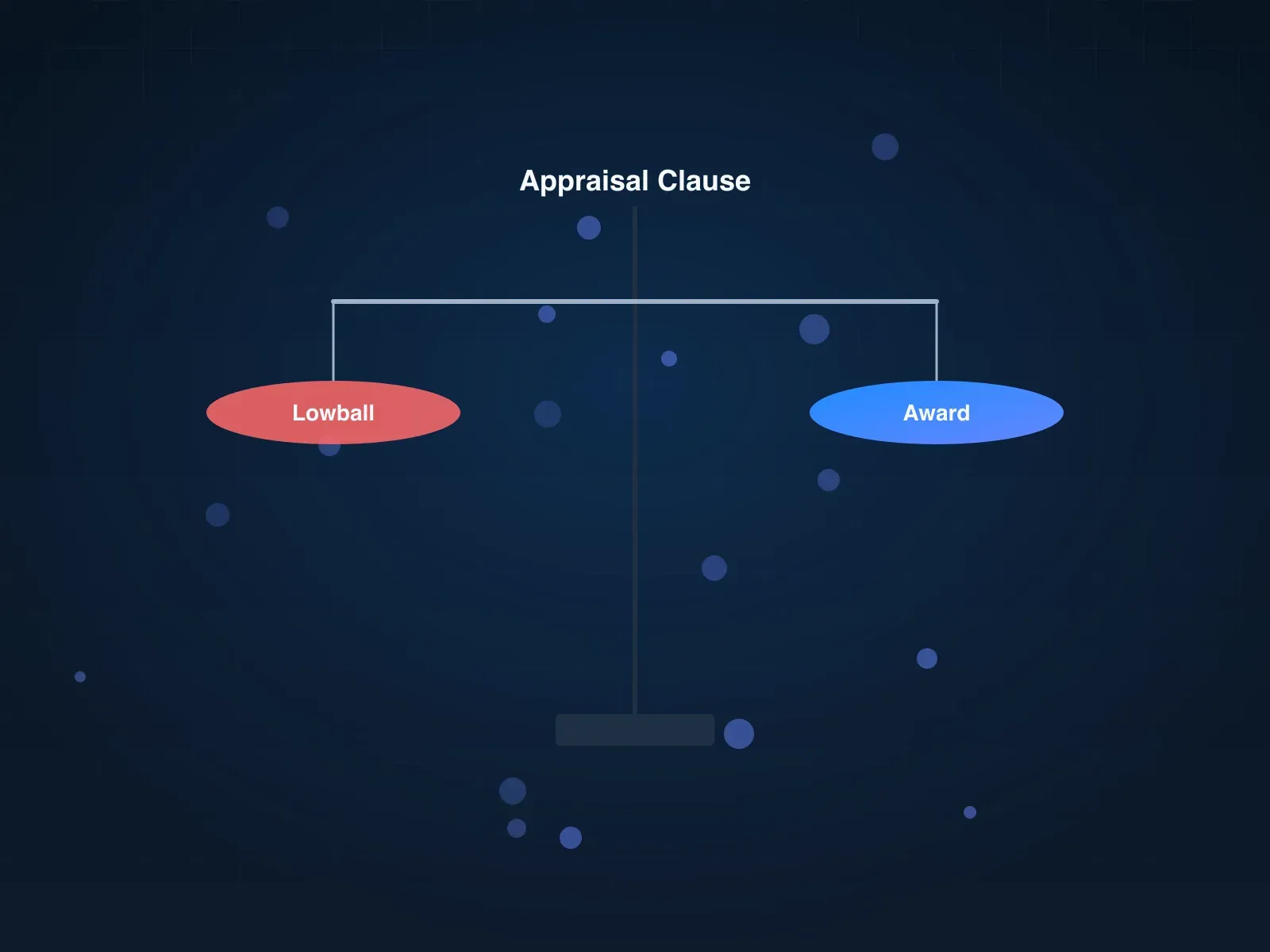

Step 5: Invoke the appraisal clause

What to do. Send a written Appraisal Demand Letter. Every standard U.S. homeowner policy has an appraisal clause. It says that if you and the carrier disagree on the amount of loss, either side can demand appraisal: each side picks an appraiser, the two appraisers pick a neutral umpire, and the binding award is whatever any two of those three agree on.

When it works and when it does not. Appraisal is for amount disputes, not coverage denials. If the carrier says “we covered it, here is your check,” and the check is way too low, appraisal is the nuclear option. If the carrier says “this is not a covered loss, go away,” appraisal will get rejected because there is no amount dispute yet. For coverage denials, you are going to step 6.

An r/homeowners regular made the distinction cleanly:

hiring a PA != ‘insurance has no choice but to pay for the entire thing’. OP didn’t disclosure their policy’s verbiage on roof replacement but, for instance, if they have an ACV policy and the roof is 20+ years old then a PA isn’t likely to get a single dollar out them. A PA will (or should, at least) get them exactly what they’re entitled to, which is significantly more than they typically pay out.

u/WarDEagle, r/homeowners thread

Template for the demand letter.

Subject: Appraisal demand, claim [#], policy [#]

Pursuant to the appraisal provision of my homeowner policy, I am invoking appraisal as to the amount of loss for claim [#] at [address]. My appraiser is [name, address, phone, credentials]. Please provide the name and contact information of your appraiser within 20 days of this letter so that the two appraisers can select a neutral umpire. I understand the resulting award will be binding as to the amount of loss.

[Signature, date] Certified mail receipt [#]

Send it certified mail with return receipt. Most policies give the carrier 20 days to name an appraiser. Realistic timelines: 30 to 60 days from demand to appraiser selection, another 30 to 90 days to walk the roof and argue line items, 15 to 30 days after that to umpire and award. Budget 3 to 6 months for a full appraisal if it goes the distance. Faster if the two appraisers settle without the umpire.

How to pick your appraiser. You want a licensed public adjuster, a retired field adjuster, or a contractor with Xactimate certification and appraisal experience. You do not want your own roofer as your appraiser. Appraisers are supposed to be competent and impartial; your roofer is neither in the eyes of the carrier, and that gets challenged. Budget $1,000 to $3,000 for your appraiser on a typical residential claim, often paid as a flat fee, sometimes as a percentage.

The Xactimate vs Symbility trap. Some carriers (Allstate, Safeco, Liberty Mutual among them, per Metro City Roofing’s field observations) use Symbility pricing, which runs around 30% lower than Xactimate for the same scope. Your appraiser should insist on Xactimate, or at minimum local-market comparables. This alone can close most of the gap.

What it costs, how long. $1,000 to $3,000 for your appraiser, 3 to 6 months, and a binding result.

Done looks like. A signed appraisal award, and the carrier writing you a check for the award amount minus your deductible.

Step 6: Hire a public adjuster or a property-damage attorney

What to do. If the carrier is denying coverage outright, if they are missing statutory deadlines (for example Florida requires a claim decision within 90 days of proof of loss under Florida Statute 627.70131), or if the case is too big for you to run yourself, bring in a licensed professional.

Public adjuster vs attorney, in one paragraph. A public adjuster is a state-licensed claims negotiator who works for you, on contingency, and takes 10% to 15% of the settlement (sometimes lower on larger claims, capped by state law in storm declarations). A property-damage attorney sues the carrier for breach of contract and bad faith. Their contingency is usually 30% to 40%, and in states with fee-shifting statutes (Florida, Texas, Colorado, Minnesota among them), the carrier can be ordered to pay your attorney fees if you win. Use a PA first for amount disputes, lowball settlements, scope fights. Use an attorney for coverage denials, egregious delay, bad-faith conduct, and anything where the carrier accused you of misrepresentation.

An active Texas public adjuster laid out the fee math for homeowners:

Before hiring an attorney that will take roughly 40% of your claim, hire a public adjuster. We can only take 10%. Most PAs lower their percentage based on claim amounts. We work on a contingency fee basis. We are the guys attorneys typically call when they need help with dispute resolution on claims.

u/Supp_Dawg95, Texas public adjuster, r/homeowners thread

The same PA shared a case example:

I had a claim for an elderly woman who had a tree cut her house in half. State Farm offered her about $7k. She was a school teacher and did not have time to deal with her insurance adjuster… I stepped in and fought the carrier and she received roughly $270,000.

u/Supp_Dawg95, Texas public adjuster, r/homeowners thread

For a more typical hail case, a homeowner on r/homeowners described the math when a PA was layered with a roofer:

My public adjuster got my entire roof and then some (gutters, screens) covered 100% by insurance, who initially was going to cover basically a box of shingles. Total bill when done was $52k. He charged 14% but all of that was absorbed by the roofing contractor since they worked together. I paid only my $1k deductible.

u/BAHGate, r/homeowners thread

How to vet a PA. State license on the state insurance department site. Years in business. Talk to two references on storm claims (not commercial or fire). A written contract that states the fee percentage, the scope, and your right to cancel (most states give you a 3-day or 72-hour rescission on PA contracts). Walk away from any PA that wants to sign you up in your living room the day after a storm. That is the PA version of a door-knocker.

How to vet an attorney. Look for a property-damage or first-party insurance lawyer with actual trial experience against your specific carrier. Ask to see two prior verdicts or settlements on hail cases in the last 24 months. Confirm the fee is contingency, the percentage, and how costs (expert witnesses, filing fees) are handled if you lose.

What it costs, how long. PA: 10% to 15% contingency, claim typically resolved in 60 to 180 days. Attorney: 30% to 40% contingency plus expenses, typically 9 to 24 months, or longer if the case goes to trial.

Done looks like. A signed engagement letter, and the PA or attorney sending the carrier a formal demand letter within the first week.

Step 7: File a Department of Insurance complaint

What to do. File a formal complaint with your state’s Department of Insurance (sometimes called the Insurance Commissioner or the Office of Insurance Regulation). This is free, done online in most states, and escalates the claim from the adjuster’s desk to a regulatory inbox the carrier actually watches.

What a DOI complaint does and does not do. A DOI complaint does not order the carrier to pay you. It triggers an investigation into whether the carrier violated unfair claim settlement practices laws: failing to acknowledge the claim in time, ignoring evidence, misrepresenting the policy, or delaying without cause. A finding against the carrier shows up in their public complaint record and can support a bad-faith suit. In practice, most carriers respond to DOI complaints by reopening the file, because the alternative is a paper trail they do not want.

One Denver-7 investigation of 40 Allstate cases found that 25% of complaints resulted in an Allstate payout of $1,500 to $26,000 after the consumer filed. The DOI had not ordered payment in those cases. The complaint itself was the lever.

What to include in the complaint.

- Your policy and claim numbers, the date of loss, and the date of denial.

- The exact denial reason, quoted from the letter.

- A chronology of every inspection, email, call, and missed deadline, dated.

- Your two independent roofer reports.

- The adjuster’s file (from step 2), marked to show what is missing or misrepresented.

- Your appraisal demand letter (if step 5 was ignored).

Timelines to expect. The carrier typically has 15 to 21 days to respond to the DOI after the complaint is filed. The DOI investigation runs 4 to 8 weeks on top of that. You will hear back by letter or email with the DOI’s findings.

What it costs, how long. $0. Six to ten weeks to a decision. If the DOI finds a violation, the carrier can face fines in addition to being told to cure the claim.

Done looks like. A DOI complaint number, the carrier’s written response, and (most of the time) a new offer or a reopened file on your claim.

Common denial reasons and the counter-move for each

| Denial phrase on the letter | What it usually means | Counter-move |

|---|---|---|

| Damage does not exceed your deductible | Carrier admits damage, underpays | Step 5: appraisal on the amount |

| Cosmetic only / cosmetic exclusion | Carrier sees impacts, denies function | Pull shingle manufacturer spec; match rule in some states (Minnesota, Iowa case law); soft-metal damage as corroboration |

| Wear and tear / aged roof | Carrier blames time not hail | NOAA Storm Events hail data for your address and date; neighbor replacements; test squares showing fresh impacts with exposed mat |

| Pre-existing damage | Carrier says damage predates policy or storm | Pre-storm aerial imagery; listing photos; last home-sale inspection; NOAA storm date timestamp |

| Hail under 1 inch does not damage shingles | Rule of thumb, not a spec | Manufacturer impact rating (GAF, Owens Corning, CertainTeed publish 1.25-inch to 2-inch thresholds that, if struck, void warranty); NOAA actual hail size for your address |

| Damage caused by wind not hail | Denying the peril, keeping coverage | Both are usually covered; ask for the carrier’s citation and the peril’s policy language. Push back with photos of impact patterns (hail = circular bruises, wind = creased tabs, lifted edges) |

| Non-compliant installation | Carrier blames roofer | Have your roofer pull the manufacturer’s install spec and show compliance |

| Biased engineer report | Often a paid report contradicting your roofer | Demand the engineer’s license, credentials, and prior clients list; file a DOI complaint citing bias |

NOAA’s public hail record is the most useful external document here. Pull the exact hail size for your address and date from the NOAA Storm Events Database and drop it into every letter and complaint. It is free, government-grade, and almost always contradicts a “hail was not severe enough” denial.

What not to do

These are mistakes every working public adjuster, field adjuster, and insurance attorney sees over and over.

- Do not cash the partial check without reading the release. Some carriers enclose language with a settlement check that, once endorsed, releases all future claims from the same date of loss. Read it, or call the adjuster and get the release terms in email, before you endorse anything.

- Do not let the roofer file the claim for you. It is your policy and your claim record. A Reddit Redditor in Chicago got caught twice by a friend who was a roofing salesman: the first claim got denied, the second got the homeowner almost dropped by State Farm. The r/Insurance consensus was blunt:

That roofing guy is no friend of yours. He’s an ambulance chaser.

u/Username_Used, r/Insurance thread

- Do not sign an Assignment of Benefits (AOB) contract with a roofer without a lawyer review. AOBs let the contractor collect directly from the insurer and, in some states, locked homeowners into scope decisions they never agreed to. Florida and several other states have restricted AOBs. If a contractor insists on one, walk.

- Do not file a third claim in five years if you can avoid it. The r/Insurance community flag on this is clear:

You’ve already filed 2 claims. If you file a 3rd, you are almost guaranteed to be non-renewed.

u/FindTheOthers623, r/Insurance thread That is the carrier’s internal math, not a law, but every homeowner who has touched their CLUE report later has seen how it plays out.

- Do not hire the first door-knocker who shows up after the storm. Out-of-state “storm chasers” send teams to a hail zone, sign contracts, and leave when the work dries up. Warranty service is a problem even if the roof looks fine on day one.

- Do not leave the inspection unattended. Every version of this story ends the same way: the homeowner was at work, the contractor met the adjuster alone, a deal was cut that nobody wrote down. Attend every inspection. Take your own photos. Get answers in writing.

- Do not agree to a carrier “preferred contractor” without checking the scope. Preferred contractors often have per-claim pricing agreements that favor the carrier, not you. Your policy lets you choose your own roofer in every state.

- Do not miss your appeal deadline. The appeal window is in your denial letter and in your policy. It runs out.

When to escalate: the decision tree

Work top to bottom. Stop at the first row that matches.

| Your situation | Best next step |

|---|---|

| Carrier admits damage, denies only the amount. Dispute is under $10K | Re-inspection + supplement, no PA needed |

| Amount dispute, $10K to $75K, single peril | Appraisal clause (step 5) |

| Amount dispute, $75K+, or multiple perils (hail + wind + water) | Public adjuster (step 6) on contingency |

| Coverage denied outright (“not a covered loss”) | Property-damage attorney (step 6) |

| Missed statutory deadlines (no response in 30, 60, 90 days depending on state) | DOI complaint (step 7) + attorney consult |

| Carrier made accusations of misrepresentation, fraud, or late notice | Attorney immediately. Do not speak to the adjuster without counsel |

| Carrier is dragging past 12 months with no resolution | DOI complaint + bad-faith attorney, simultaneously |

Most homeowners resolve at steps 4 and 5. The ones who need 6 and 7 usually know it, because the denial letter reads like a legal brief, not a claim decision.

Key takeaways

- Your appeal window is 60 to 180 days. Calendar it the day you open the letter.

- Get the denial in writing, with the policy language cited. Everything else is guesswork without it.

- Two independent roofer reports plus 10 by 10 test squares on three or four slopes is the evidence baseline. Soft-metal damage decides close cases.

- The appraisal clause is your strongest, cheapest lever when the carrier admits damage but lowballs the amount. The award is binding.

- PAs take 10 to 15%; attorneys take 30 to 40% plus fee-shifting in some states. PA for amount disputes, attorney for coverage denials.

- DOI complaints are free and carriers respond to them more than they admit. File one if deadlines slip.

- Never cash a partial check without reading the release, never sign an AOB, and never leave an inspection unattended.

FAQ

How do I dispute an insurance claim denial on my roof?

Send a written appeal within your policy’s appeal window (typically 60 to 180 days), attach two independent roofer reports with test-square photos, and request a re-inspection with your roofer present. If the carrier still refuses to move, invoke the appraisal clause in your policy for amount disputes, or file a DOI complaint and hire a property-damage attorney for coverage denials.

What should I do if insurance denied my roof claim?

Work the seven steps in order: save the denial letter, request the full adjuster file, get two independent roofer inspections, file a re-inspection, invoke appraisal, hire a public adjuster or attorney, file a state DOI complaint. Do not cash any partial check until you understand the release language on it, and do not sign an AOB contract with a roofer.

How many claims before insurance drops you?

Most carriers flag homeowners after two claims in a rolling three- to five-year window, and a third claim in that window almost always triggers non-renewal. Weather-driven hail and wind claims count, even when paid at policy limits. Every claim, paid or denied, shows up on your CLUE report and is visible to every carrier you later apply to.

Can you sue insurance for denying a roof claim?

Yes. A property-damage attorney can sue your insurer for breach of contract, and in many states (Florida, Texas, Colorado, Minnesota among them) also for bad faith, which can trigger attorney-fee shifting and, in some cases, extra-contractual damages. The case usually takes 9 to 24 months and runs on contingency, so you only pay if you recover.

How long do I have to appeal a denied hail damage insurance claim?

Most policies give you 60 to 180 days from the denial date to file a formal appeal, but the appraisal clause and any statute of limitations run on a separate clock (often 1 to 5 years from the date of loss). Read both the denial letter and the policy’s “Duties After Loss” section and mark every deadline on a calendar the same day you get the letter.

Does filing a hail claim raise my home insurance?

Filing a claim does not raise your rate during the current policy period, but it can raise your renewal premium or cause non-renewal, especially if you already filed in the last three to five years. Pure weather claims (hail, wind) typically have less rate impact than liability claims, but every paid claim shows up on your CLUE report.

What is a 10 by 10 test square and why does my adjuster keep talking about it?

A 10 by 10 test square is a chalked-off 100-square-foot area on your roof where every hail impact inside the box is circled and counted. Carriers use it to estimate hits per square across the whole roof. Allstate and State Farm want to see test squares with real hail hits on at least three to four slopes before approving a full roof replacement. Soft-metal damage on gutters, vents, and flashing supports the test-square count.

What is the difference between a public adjuster and a property-damage attorney?

A public adjuster is a state-licensed claims negotiator who works for you on contingency (10% to 15%) and handles scope and amount disputes with the carrier. An attorney files a lawsuit for breach of contract or bad faith and typically takes 30% to 40% plus costs, with fee-shifting available in some states. Use a PA for amount, scope, and lowball settlements; use an attorney for outright coverage denials, missed deadlines, or accusations of fraud.

How do I invoke the appraisal clause on my insurance policy?

Send a written Appraisal Demand Letter by certified mail, name your appraiser, and cite the appraisal provision in your policy. The carrier then names its appraiser; the two jointly pick a neutral umpire; any two of the three can issue a binding award on the amount of loss. Most appraisals resolve in 3 to 6 months and cost the homeowner $1,000 to $3,000 for the appraiser.

Can I get a new roof if my neighbor did?

Maybe, but it depends on your own roof’s damage, not theirs. Neighbors getting new roofs is a useful signal that hail was in the area, and Allstate agents have confirmed adjusters look at neighbor claims, but you still have to document 10 by 10 test squares on three or four of your own slopes plus soft-metal damage. Photos of your neighbor’s replacement plus NOAA hail-size data for your shared address belong in your claim file.

Should I cash the partial settlement check before the claim is resolved?

Not until you read the release language and confirm in writing that endorsing the check does not release the rest of your claim. Some partial checks are “partial indemnity” and preserve your right to supplement. Others are “full and final” and close the claim when you deposit them. Ask the adjuster for the release terms in email, and if in doubt, have a public adjuster or attorney review before you endorse.

Related reading

- Carrier-specific: Allstate denied my roof claim and State Farm denied my roof claim

- Denial template: hail under one inch denial

- Action guide: how to invoke the appraisal clause

- Decision guide: public adjuster vs attorney

- Cost fight: Xactimate estimate gap audit

- Before you file: CLUE report and non-renewal risk

- Documentation: hail damage evidence checklist

- Contractor vetting: how to hire an honest roofer

Ready to build your claim file the way a working public adjuster would? Generate your free pre-storm satellite imagery report with NOAA hail-size data for your exact address and date. It takes 2 minutes and becomes evidence you can hand to the adjuster, your roofer, or an attorney.