Two hours after a hailstorm, someone will knock on your door. Clipboard, company polo, free inspection. If you say yes without the right questions, the best case is a rushed repair that ends up as a denial on your CLUE report. The worst case is a contractor who damages your roof on purpose, pockets your deductible, and disappears when the carrier denies a claim you didn’t know you were filing. Here’s the 8 questions to ask before you sign, the door-knocker refusal script, and the difference between a local roofer and a storm chaser.

TL;DR (the four moves)

- Don’t sign anything on the doorstep. Use the 3-question refusal script first.

- Verify license + COI on the state website before anyone climbs the roof. License + COI in your inbox within 24 hours, or it’s a no.

- Ask the 8 vetting questions before signing. Q7 (commission if denied) and Q8 (deductible-eating) are auto-declines.

- Get the full Xactimate scope in writing before signing. “Sign first, scope later” is the blank-contract AOB trap.

Average vetting time: 30 minutes of phone calls and two website lookups. Average cost of hiring a storm chaser: the deductible, the rest of the roof, plus non-renewal risk.

Why the roofer you hire decides the claim

Roofing in a hail-belt state operates in two tiers. Local contractors install year-round and treat claims as secondary revenue. Storm chasers are out-of-state sales crews who follow weather reports, knock neighborhoods, and file as many claims as they can before moving on.

Red flags are out-of-state companies and door knockers. Never go with a national company unless they have a legitimate office in your area. A lot of times they send 10 salesmen out to a storm area and leave once the work dries up.

u/GayNotGayTony, r/Roofing thread

The storm is the product, the roof is the vehicle, and your signature is what gets paid. The fix starts at the doorstep.

Step 1: The door-knocker refusal script (first 48 hours)

Hailstorms create a 24-to-72-hour window where door-knockers saturate hit neighborhoods. Your job isn’t to pick a roofer. It’s to close the door on storm chasers without giving up a signature.

Q1: “Do you have a local office within 30 minutes’ drive?” Local roofers have an actual office, landline, yard with trucks, permanent address. Storm chasers rent short-term space or list a virtual mailbox. Vague, out-of-state, or “we’re mobile” = close the door.

Q2: “Can you email your state contractor license number and COI right now?” Licensed contractors have both on their phone. Honest answer arrives in your inbox while you’re standing at the door. “Check with the office” or “bring it next time” means they don’t have either. Texas, Colorado, and Missouri don’t require a state-wide roofing license (municipal licenses and GC bonds apply); most other states do.

Q3: “What’s your written refund policy if I cancel within 72 hours, and your charge if insurance denies?” Legitimate contractors have a written 3-day cancellation policy (federal FTC Cooling-Off Rule requires it) and charge zero on denial. Storm chasers evade or say “it’s negotiable.”

The core rule. Never sign anything on the doorstep. Never let anyone climb the roof the same day they knocked. Three “yes” answers isn’t a booking; it’s permission to verify. Check the license on the state website and call the COI carrier before you open the gate.

Done looks like. Door closed on any salesperson who can’t answer all three. Any “yes” answers saved in a text thread for later verification.

Step 2: The 8 vetting questions before you sign

Once you have 2 to 3 roofers from the door-knocker script or neighbor referrals, run the full vetting pass. Every question has a pass/fail criterion; Q7 and Q8 are auto-declines on a single wrong answer.

Q1: How long have you operated under this business name, at this address?

Pass: 3+ years with a verifiable local office. Fail: under 3 years or out-of-state mailing address. Storm-chaser entities rotate names every 18 to 24 months to shed bad reviews and unfulfilled warranties. An 18-month-old LLC can’t warranty a 30-year roof.

Q2: Can you send me your state contractor license and COI?

Pass: both in your inbox within 24 hours, with GL AND workers’ comp. Fail: evasive, delayed, or missing workers’ comp. Call the carrier on the COI to verify the policy is active today; storm chasers frequently use expired COIs. No workers’ comp means you’re personally liable if a worker falls on your property.

Q3: Do you have a dedicated supplements role?

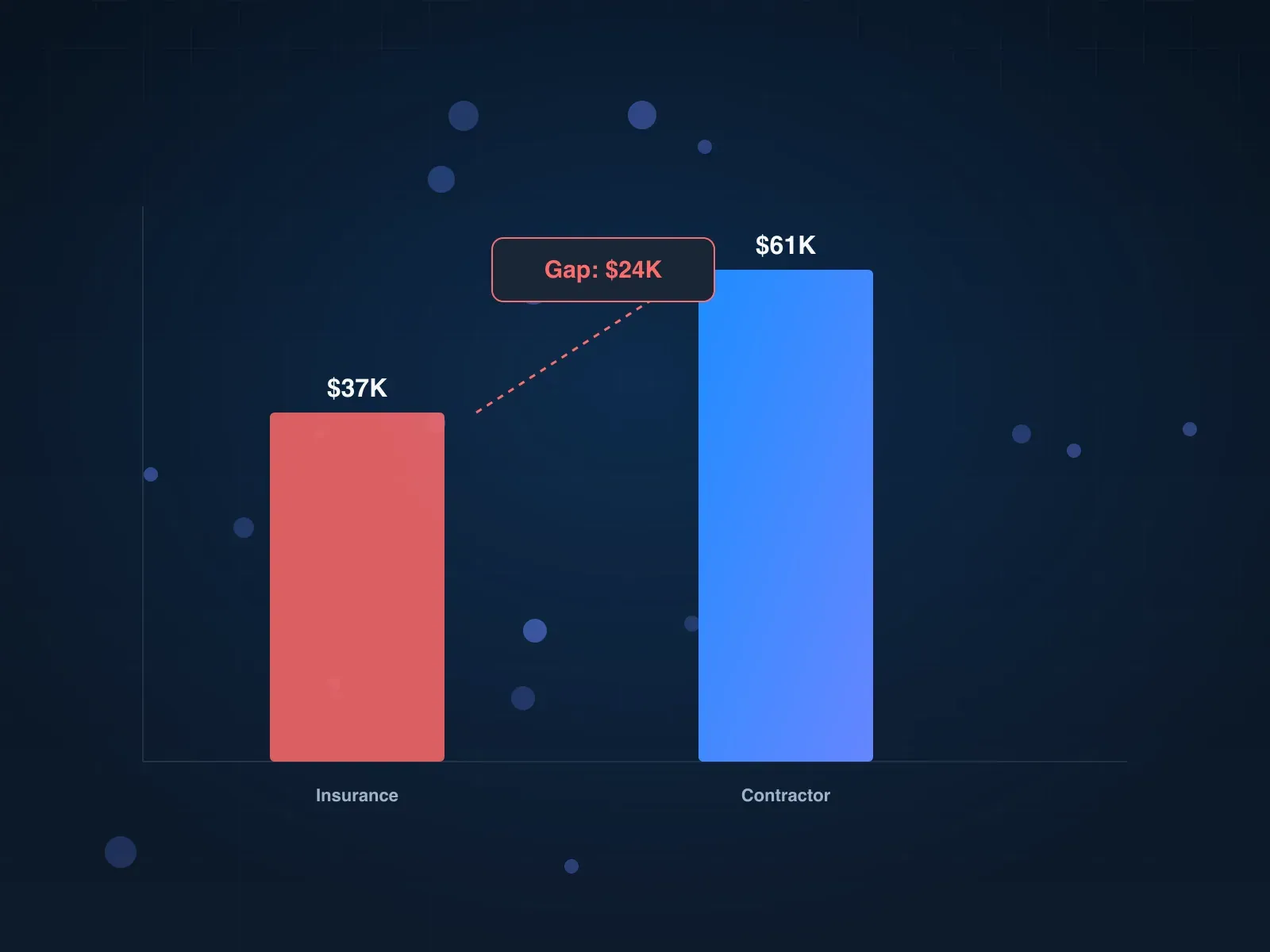

Pass: a named employee handling supplementals full-time. Fail: “we leave that to the insurance company.” A supplements role is the difference between a $37K carrier offer and a $61K payout (see the Xactimate gap audit guide).

Q4: What is your manufacturer certification level?

Pass: GAF Master Elite, Owens Corning Platinum Preferred, CertainTeed SELECT ShingleMaster, or equivalent tier-1 certification. Fail: no certification. Certification determines warranty length (25 to 50 years on labor + materials) and requires manufacturer installation standards. An uncertified installer voids the warranty, and if installation fails in year 5, the homeowner eats the repair.

Q5: Will you absorb the public adjuster fee if I hire one?

Pass: yes, with terms in writing. Fail: no, or no mention of PA partnership. Good roofers partner with PAs on complex claims because the PA gets the scope to full replacement, the roofer wins a larger job, and the homeowner doesn’t pay out of pocket. One r/homeowners case flipped a “box of shingles” offer into $52K when the contractor absorbed the PA’s 14% fee (r/homeowners thread).

Q6: Can you show me the full Xactimate scope before I sign anything?

Pass: yes, as a PDF before signing, line items matching the verbal walk. Fail: “sign first, scope later.” That’s a blank contract that gets filled as an AOB. The structure that protects both sides: exclusivity in exchange for a full Xactimate scope.

Q7: What’s your commission if my claim is denied? (auto-decline)

Pass: zero, in writing. No deposit kept, no cancellation fee, no administrative charge. Fail: deposit retained, flat fee, or “we’ll discuss if it comes to that.” Legitimate contractors don’t invoice until the carrier approves. Storm chasers get paid on signature.

Q8: Will you eat my deductible? (auto-decline)

Pass: no, and they refuse. Fail: yes, or any variant of “we’ll work with you,” “we’ll absorb it,” “no out-of-pocket for you.” Waiving or “eating” a deductible is insurance fraud in all 50 states. The contractor pads the estimate; the homeowner commits fraud by participating. If caught, you face policy cancellation, non-renewal on CLUE, and potential criminal charges. Close the conversation.

Done looks like. 2 to 3 roofers who passed all 8 questions, each with a full written Xactimate scope, signed COI on file, and cancellation policy you can read.

Step 3: Verify license and insurance on the state website

Don’t take the roofer’s word for license or insurance. Verify both independently.

License. Google “[your state] contractor license search” or “[your state] secretary of state business search.” Check license status (active, expired, suspended), issue date, and disciplinary actions. Texas, Colorado, and Missouri don’t require state roofing licenses; look up the business entity and municipal registrations.

Insurance. Read the COI. Note carrier, policy number, and expiration. Call the carrier directly (Google the main line, not the COI number) to verify the policy is active and both GL and workers’ comp are current. Workers’ comp is the critical one: GL covers damage to your property, workers’ comp covers injury to their crew on your property.

Bond. Florida, California, and parts of Texas require roofing bonds. The bond number is on the COI or state record. A current bond gives you recourse if the contractor takes a deposit and disappears.

Done looks like. A screenshot of the state license page and a call to the COI carrier confirmed, dated and saved.

Step 4: Contract red flags before you sign

Four clauses to find (and refuse) before signing:

1. AOB. An Assignment of Benefits transfers your right to file and collect on the claim to the contractor. They file, communicate with the carrier, and bank the check; you lose control and often can’t fire them. Florida banned new AOBs in 2019. If the contract has one, strike it, initial, and confirm in writing. If the contractor refuses, walk.

2. Blank or incomplete scope. Every line item, quantity, material, and price should match the Xactimate scope from Q6. Blank lines (“to be determined,” “per insurance scope”) mean the contractor fills in whatever they want after you sign.

3. No cancellation clause. The FTC Cooling-Off Rule gives you 3 business days to cancel any in-home door-to-door contract, no penalty. The contract must disclose this and include two cancellation forms. If it doesn’t, find a contractor whose paperwork is legal to begin with.

4. Vague insurance-contingency language. Some contractors write “contract is contingent on insurance approval” in a way that traps homeowners on partial approvals. Cleanest language: “If insurance doesn’t approve full replacement, homeowner may cancel within 7 days of final carrier estimate, no penalty.” Negotiate it in before signing.

Done looks like. A fully populated contract, valid cancellation clause, no AOB, no blank scope, clear contingency terms.

Step 5: Verify reviews aren’t fake

Fake reviews are the storm chaser’s growth hack; a new LLC can post 30 five-star reviews in a week.

Real signals. Specific local details (street names, roofer names, project photos), review history older than 12 months, reviewer profiles with other local businesses in your metro, review text that varies in length and tone.

Fake signals. A cluster of 5-star reviews within a 7-day window, one-line “Great service!” with no specifics, reviewers whose profiles only rate home-improvement businesses in multiple states, 50 Google reviews but no Facebook or BBB history.

Where to cross-check. Google, BBB (complaint history not just rating), Facebook (harder to fake), Nextdoor (neighbors who just got roofs installed are the best source), state Attorney General complaint database.

Call 3 references from the last 6 months. Ask for homeowner name, address, and phone (not a stock reference). Ask: “Was final cost close to the contract? Did they handle supplements? Any surprises?”

Done looks like. 3 to 5 review sources checked, 3 reference calls completed.

Local established roofer vs storm chaser: the matrix

One match on insurance coverage, deductible-eating, or refund policy is enough to fold. The hailstorm hands the storm chaser an urgency advantage; your job is to refuse to be rushed.

The “everyone is getting approved” tell

“Everyone is getting approved” is the most reliable storm-chaser tell. Not every storm produces covered damage, not every roof qualifies, and the non-renewal threshold is 3 claims in 5 years (see the CLUE-report pre-filing guide). The only homeowners who all get approved are the ones whose contractors damaged the roofs on purpose, and carriers catch that pattern fast. A Chicago homeowner filed twice on a “friend” adjuster’s advice, got denied both times, and nearly lost his State Farm policy on the third attempt (r/Insurance thread).

What not to do

- Don’t sign anything on the doorstep. FTC Cooling-Off gives you 3 days; it’s faster to just not sign.

- Don’t let any contractor climb the roof the same day they knock. Verify license and insurance first.

- Don’t sign an Assignment of Benefits. If the contract has one, strike it, initial, and confirm in writing.

- Don’t take a roofer’s word on license or insurance. Call the state, call the COI carrier.

- Don’t hire a roofer who offers to waive or absorb your deductible. Fraud in all 50 states; you go down with them.

- Don’t skip the 3 reference calls. Real references from neighbors beat any Google rating.

- Don’t believe “everyone is getting approved.” Filing a weak claim costs more than it pays (see the file-or-fold tree).

Key takeaways

- Use the 3-question door-knocker script before you schedule any inspection: local office, license + COI now, written refund policy.

- Ask the 8 vetting questions before signing. Questions 7 (denial commission) and 8 (deductible eating) are auto-declines.

- Verify contractor license on the state website and COI by calling the named carrier directly.

- Refuse any contract with an AOB, blank scope, missing cancellation clause, or unclear insurance-contingency language.

- Cross-check reviews across Google, BBB, Facebook, and Nextdoor. Call 3 references from the last 6 months.

- A single storm-chaser attribute is enough to fold. Insurance coverage, deductible-eating, and refund policy are the most important rows.

- “Everyone is getting approved” is a storm-chaser tell. Non-renewal threshold is 3 claims in 5 years.

FAQ

What questions should I ask a roofer after hail damage?

Ask 8: time in business (3+ years), state license and COI emailed within 24 hours (GL + workers’ comp), dedicated supplements role, manufacturer certification (GAF Master Elite or equivalent), PA fee absorption, full Xactimate scope before signing, commission if denied (zero), and whether they will eat your deductible (only correct answer: no). The last two are auto-declines.

How do I spot a storm-chaser roofer?

Door-knocks unannounced; no local office or uses a virtual mailbox in another state; business entity under 18 months old; GL insurance only, no workers’ comp; no manufacturer certification; pushes same-day signing; offers to waive your deductible; thin review history with generic 5-star one-liners from out-of-state reviewers. A single match is enough to walk.

Is it legal for a roofer to eat my deductible?

No. Insurance fraud in all 50 states, often a felony for both the contractor and the homeowner. The contractor pads the estimate by the deductible amount; the homeowner commits fraud by participating. If caught, you face policy cancellation, a non-renewal flag on CLUE, and potential criminal charges.

How do I verify a roofer’s license and insurance?

Google “[your state] contractor license search” or “[your state] secretary of state business search.” For insurance, read the COI for carrier name and policy number, then call the carrier directly (Google the main line, not the COI number) to verify the policy is active and covers both GL and workers’ compensation.

What is an Assignment of Benefits, and why shouldn’t I sign one?

An AOB transfers your right to file and collect on the claim to the contractor. They file, communicate with the carrier, and bank the check; you lose control and often can’t fire them. Florida banned AOB contracts in 2019 after carriers hemorrhaged money to AOB litigation. If the contract contains one, strike it before signing.

How long should a roofer have been in business before I hire them?

At least 3 years under the same business name at the same address. Storm-chaser entities rotate LLC names every 18 to 24 months to shed bad reviews and unfulfilled warranties. The warranty on a new roof is 25 to 50 years; an 18-month-old LLC can’t stand behind that.

What does “show me the scope before I sign” mean?

The roofer sends a complete Xactimate estimate as a PDF, with every line item (shingles, underlayment, ridge cap, drip edge, IWS, flashing, gutters, detach-and-reset, O&P), before you sign. Line items should match the walk. “Sign first, scope later” is the blank-contract trap.

Do I need to check a roofer’s bond?

Depends on the state. Florida, California, and parts of Texas require roofing contractor bonds; most others don’t. Where required, the bond number is on the COI or state license record. A current bond gives you recourse if the contractor takes a deposit and disappears.

How do I know if a roofer’s reviews are fake?

Watch for clusters of 5-star reviews within a 7-day window, one-line reviews with no specifics, reviewers whose profiles only rate home-improvement businesses in multiple states, and businesses with 50 Google reviews but no Facebook or BBB history. Cross-check Facebook (harder to fake), Nextdoor, BBB, and state AG databases.

Should I get multiple roofer bids after hail damage?

Yes. Three bids is the standard, each with a full Xactimate scope, a COI (GL + workers’ comp), and 3 local references. The cheapest bid is rarely the right one; the bid closest to the carrier’s Xactimate number with a dedicated supplements role usually is.

What’s the difference between a roofer and a roofing salesman?

A roofer installs roofs. A salesman signs contracts and collects commissions. Storm-chaser crews hire salesmen (often kids with a week of training) who call any abnormal shingle wear “hail damage” and push homeowners to sign. The installer who shows up later is a subcontractor.

Related reading

- hail damage insurance claim denial playbook (master hub)

- Allstate denied my roof claim

- State Farm roof claim denial guide

- hail under 1 inch denial dispute

- invoke the appraisal clause

- public adjuster vs attorney

- Xactimate estimate gap audit

- CLUE report before you file a hail claim

- hail damage evidence checklist

Ready to vet your shortlist? Generate a 3-roofer comparison worksheet with the 8 questions pre-filled, state license lookup URL, and a reference-call script.