If your carrier admits there was hail damage but cut the check at a fraction of your roofer’s scope, you’re in an amount dispute, not a coverage denial. Every standard U.S. homeowner policy includes an appraisal clause that lets you force a binding third-party valuation. It’s faster than litigation, cheaper than a public adjuster on contingency, and it works. Scott Friedson, the multi-state licensed public adjuster who runs Insurance Claim Recovery Support, has documented settlements increasing 30% to 3,800% after appraisal on cases where the homeowner initially tried to handle the dispute alone. Here is how to invoke the appraisal clause the way a working PA does.

TL;DR (the five moves, in order)

- Send a written Appraisal Demand Letter by certified mail to the claim handler and the carrier’s legal department.

- Pick a competent, impartial appraiser. Not your roofer. Budget $1,000 to $3,000 as a flat fee.

- Let the two appraisers pick a neutral umpire. If they can’t agree, most state statutes let a court appoint one.

- The two appraisers walk the roof, scope the loss, and negotiate pricing. Any two of the three (two appraisers or one appraiser plus the umpire) issue a binding award.

- If the carrier still has not completed a re-inspection, fold it into the appraisal timeline. Do not wait on re-inspection before you demand appraisal.

Plan 3 to 6 months from demand letter to check. Plan 6 to 12 months if the carrier drags past statutory response windows.

Why the carrier’s check is so much lower than your roofer’s

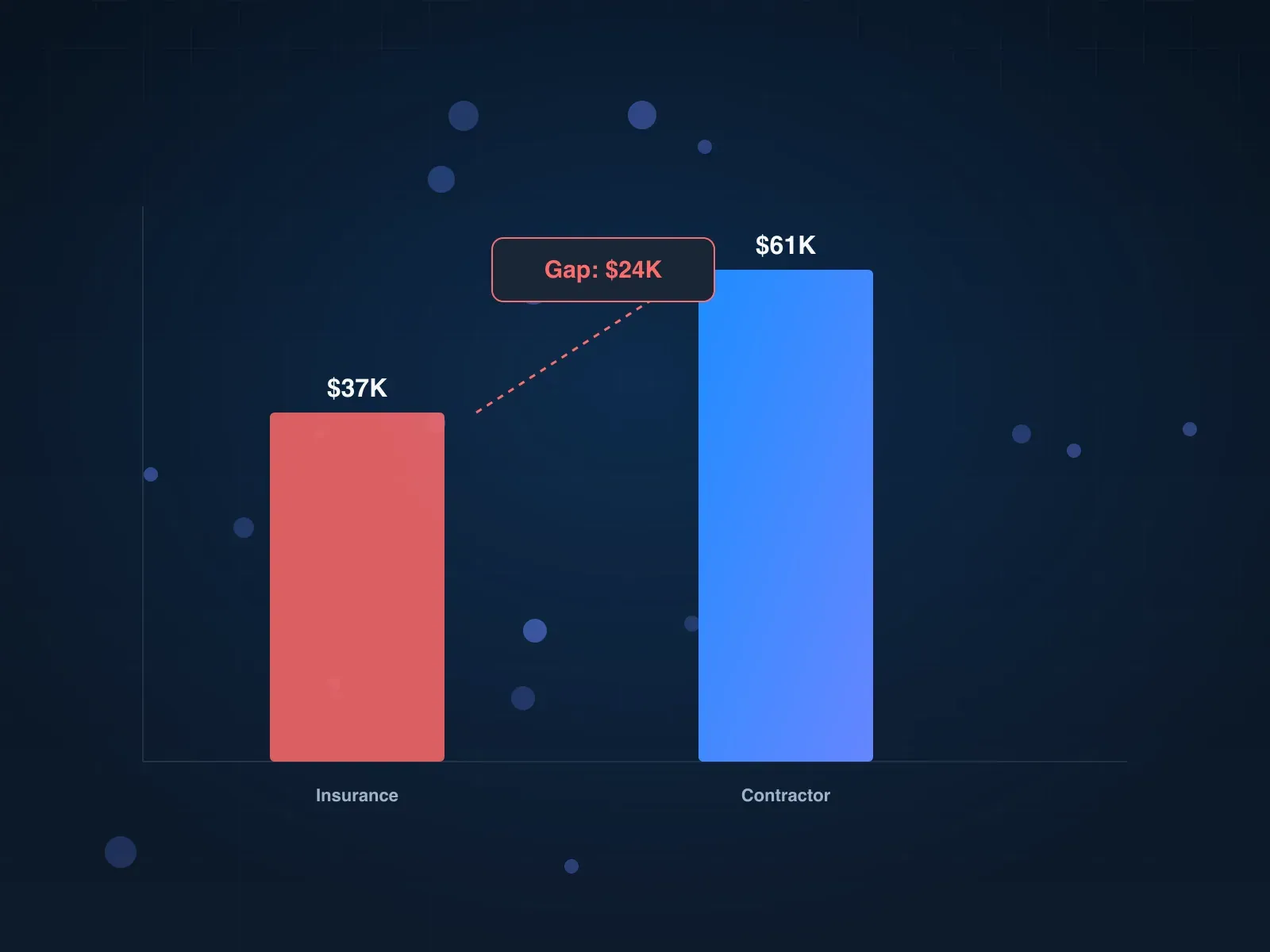

Both sides write estimates in the same software (Xactimate most commonly, or Symbility on some carriers), but the carrier’s version routinely leaves out line items worth tens of thousands of dollars. An r/HomeInspections homeowner who pushed back on a State Farm scope described the gap he closed:

Insurance gave me a $37K price. Roofing company came back at $61K. Insurance and roofing companies use the same estimation software. Insurance left a lot of things out. Roofing Co. was thorough. Insurance had no choice but to honor the Roofing Cos. estimate.

u/mrkprsn, r/HomeInspections thread

A 65% gap on the same software, closed by a homeowner walking through the line items the carrier omitted. That is what appraisal forces. The panel can’t reject a legitimate scope; it has to pick a dollar number that matches the damage on the roof. Carriers using below-market pricing software go on the record admitting they are playing volume: most homeowners never invoke appraisal, so the carrier wins by default. The ones who do invoke win more often than they lose.

Before you invoke: amount dispute vs coverage denial

Appraisal settles how much. It doesn’t settle whether. If your denial letter reads “below your deductible,” “the scope submitted is overstated,” “you are entitled to this amount, not the amount your roofer quoted,” or something similar, you’re in an amount dispute. Appraisal is built for that.

If your denial letter reads “no covered damage,” “this peril is excluded,” “you filed past the policy deadline,” or “pre-existing damage” as an outright rejection, you’re in a coverage dispute. Appraisal can’t fix that. You need an attorney and a DOI complaint, covered in the master pillar playbook.

The rest of this guide assumes you’re in the left column.

Step 1: Send the Appraisal Demand Letter

What it is. A one-page written notice that formally invokes the appraisal provision in your policy. Every standard HO-3 and HO-5 policy includes it. Metro City Roofing, a Denver contractor that handles a heavy volume of State Farm and Allstate claims, frames the mechanics:

The appraisal process begins by signing and submitting an Appraisal Demand Letter (ADL) to the insurance company. Once receiving the Appraisal Demand Letter, the insurance company has a finite timeline to review the request and select its appraiser under the insurance policy terms.

Per Metro City Roofing’s appraisal clause guide

Template.

Subject: Appraisal demand, claim [#], policy [#]

Pursuant to the appraisal provision of my homeowner insurance policy, I am invoking appraisal as to the amount of loss for claim [#] at [property address]. My appraiser is:

[Name] [Company, if applicable] [Address, phone, email] [Licensing or credential: public adjuster license number, Xactimate certification, or adjuster license]

Please provide the name and contact information of your selected appraiser within 20 days of this letter so the two appraisers can jointly select a neutral umpire. I understand the resulting award will be binding on both parties as to the amount of loss.

I am also enclosing my roofer’s complete Xactimate scope and photographs of the damage for your appraiser’s file.

Sincerely, [Your name, date] Policy [#], claim [#] Sent via certified mail, return receipt [#]

How to send it. Certified mail with return receipt to the claim handler of record and the carrier’s legal or claims department. Send the same letter as email, same day, so you have two dated delivery records. Save both the certified receipt and the email send confirmation.

Response window. Most policies require the carrier to name an appraiser within 20 days of receipt of your ADL. Some state statutes extend or compress that window (Texas runs around 20 days, Florida 60, Minnesota is governed by Quade v. Secura case law at 30 days). If the carrier misses the deadline, send a follow-up letter citing the missed deadline as evidence for a state DOI complaint.

Done looks like. The certified receipt in your file, the carrier’s written acknowledgment of receipt, and the carrier’s appraiser’s name and contact information in writing.

Step 2: Pick your appraiser

Who qualifies. An appraiser must be “competent and impartial” (policy language, enforceable). Competent means they have walked insurance claim roofs and can produce a scope in Xactimate line items. Impartial means no financial interest beyond their flat fee.

Good options.

- A licensed public adjuster in your state with appraisal experience.

- A retired carrier field adjuster who now consults or does appraisals independently.

- A Xactimate-certified contractor who does appraisal as a separate service line (not the contractor who will do the repair).

- A HAAG-certified roof inspector with an engineering background.

Bad options. Your roofer. Per an ICRS guide:

Selecting an appraiser is critical. You want someone with specific experience in insurance appraisals and knowledge of your type of damage. Don’t just pick any contractor, choose someone who understands the appraisal process and can present compelling evidence of damage values.

Per Insurance Claim Recovery Support, a national public adjuster firm (Scott Friedson)

Carrier appraisers reliably challenge homeowner-roofer appraisals for impartiality, and umpires sometimes side with the carrier on that single ground.

Cost. $1,000 to $3,000 flat, paid by you. Some charge a percentage of recovery (2% to 5%), but most decline contingency because it creates the same impartiality problem.

Credentials to ask about. State PA license (required in most states to negotiate amount disputes), Xactimate certification, appraisal experience in your state and with your carrier. Ask for two references on prior appraisal cases inside the last 24 months.

Done looks like. A signed engagement letter, license and Xactimate certification on file, and contact info ready to send to the carrier.

Step 3: Umpire selection

What the umpire does. The umpire is the tie-breaker. If your appraiser and the carrier’s can’t agree, the umpire reviews each position and picks one. The umpire doesn’t split the difference and doesn’t write a new number. Per Metro City:

The two appraisers and the umpire are known as the appraisal “panel.” From there, agreement by any two of the three appraisal panel members will finalize the extent of loss and set the financial coverage amounts.

Per Metro City Roofing’s appraisal clause guide

How the umpire is picked. The two appraisers jointly propose candidates and agree on one. If they can’t agree within a policy-specified window (often 15 or 30 days), most state statutes let a court appoint the umpire on motion in the county where the property sits.

Who should be an umpire. Retired insurance adjusters, retired property-damage attorneys, Xactimate-certified independent consultants, and licensed PAs who don’t work directly for either side. Vet the candidate’s prior appraisal history; patterns of siding with one side are a conflict.

Cost. $1,500 to $5,000 for the umpire, split 50/50 per standard appraisal provisions. Some policies require the loser to pay the umpire; check yours.

Done looks like. A written umpire engagement, credentials on file, and a scheduled date for the panel inspection.

Step 4: The binding award process

The walk. Both appraisers (sometimes the umpire) visit the property together. Each side brings prior positions: the carrier brings the adjuster’s Xactimate or Symbility scope; you bring your roofer’s scope. They walk the roof, mark damage, and photograph each disputed line item.

The scope and pricing fight. Two things get fought at every appraisal:

-

Scope. Which roof elements are damaged and need replacement vs repair. Soft metals, ridge and starter courses, flashing, detach-and-reset, and interior water damage are the usual disputes.

-

Pricing. Xactimate vs Symbility is the most common pricing fight. Metro City’s field observation:

We are experiencing that Symbility prices its claims approximately 30% less than Xactimate.

Per Metro City Roofing

The carrier’s appraiser often defaults to Symbility; your appraiser should insist on Xactimate or local-market comparables. The umpire decides.

What Shelter Insurance admitted. Metro City documents a Symbility-using carrier going on the record:

Insurance companies like Shelter Insurance that use Symbility shared that they understand the under-market pricing and are prepared to go to appraisal when pressed. They know they will lose most of the time but win some of the time.

Per Metro City Roofing

Translation: carriers using below-market pricing software are playing a volume game. Most homeowners never invoke appraisal, so the carrier wins by default. The ones who do invoke appraisal win more often than they lose.

The award. When two of three panel members agree, the award is set. The binding award letter states the amount of loss in one number; the carrier is contractually obligated to pay that minus your deductible within the state payment window (typically 30 to 60 days).

Real case, real numbers. A Denver State Farm claim in 2021: the initial adjuster was on the roof under 60 seconds before denying shingles as “not hail.” The carrier re-inspected and still denied shingles but marked 19 roof vents plus gutters, downspouts, window screens, and garage doors. The homeowner sent an ADL. The two appraisers met, agreed the roof had extensive hail damage, and approved the full replacement. No umpire needed.

When the carrier drags. A documented YouTube case ran 18 months from storm to approved claim: 3 months for the carrier to name an appraiser, 10 months to the first meeting, and even after the carrier’s own appraiser agreed the roof needed replacement, 2 more months for the report to land, then a shingle obsolescence test, then more delay, until the homeowner threatened a bad-faith claim at month 17 and got approval days later. Contractor narration on the field video:

The links to which this insurance company was going to deprive this homeowner of the benefits of his insurance coverage was just something that I’d never seen before.

Contractor narration in DENIED! Homeowner Takes On Insurance Company For A New Roof

If your appraisal drags past 9 months, run a bad-faith attorney consult in parallel. Extended silence after your appraiser produced a scope is itself actionable.

Done looks like. A signed award letter, the carrier’s check in your account (award minus deductible), and a clean invoice history from your appraiser.

Step 5: Fold re-inspection into the appraisal timeline

The trap. Most homeowners think they’ve got to run the carrier’s re-inspection first, let it fail, then invoke appraisal. Metro City’s position:

At Metro City Roofing, we work with homeowners to demand appraisal less than 10% of the time.

Per Metro City Roofing

Metro City uses appraisal as a last resort, and so should you. But the timing works against you if you run re-inspection, wait 30 to 60 days, let it fail, and only then start the 3 to 6 month appraisal clock. That puts you past most state statutes of limitation on hail claims.

The fix. Send the ADL and the re-inspection request at the same time, with language that lets the carrier withdraw one by meeting the other:

I am also requesting a re-inspection of the property by a different field adjuster within the next 14 days. If the re-inspection produces an acceptable revised offer, I will withdraw this appraisal demand in writing. Otherwise, please proceed with naming your appraiser in accordance with the policy.

That paragraph protects both paths. If the re-inspection produces a revised offer close to your roofer’s scope, you drop the appraisal. If it comes back with the same number, the appraisal clock is already running.

Budget the full cycle. Plan 3 to 6 months from ADL to check. Plan 6 to 12 months if the carrier misses response windows or pushes obsolescence tests, shingle lab reports, or engineering reports. Above 12 months, you have a bad-faith case running in parallel.

Done looks like. A single intake folder with ADL, re-inspection request, both responses, appraiser engagement, umpire engagement, and award letter in chronological order. That folder is what an attorney asks for on day one if the appraisal itself falls apart.

Common carrier objections at appraisal and the counter for each

Once the appraisal is running, expect the carrier’s appraiser and claim handler to push back on the same set of items every time. Know the counter before the walk.

| What the carrier’s appraiser says | What they mean | Counter-move |

|---|---|---|

| ”Symbility pricing is the industry standard” | Their software runs ~30% below Xactimate on the same scope | Insist on Xactimate or local-market comparables; the umpire decides |

| ”The scope you submitted is overstated” | They are rejecting specific line items, not the roof | Ask them to mark the specific line items; argue each one individually |

| ”Ridge and starter are already covered in the square cost” | Trying to cut named line items as duplicative | Cite the Xactimate line-item definitions; ridge and starter are separate |

| ”5% waste factor is our standard” | Default software setting, not field reality | On a gable roof, waste often runs 18%; provide photos of the cut pattern |

| ”Detach and reset on soft metals is not payable” | Excluding a standard Xactimate line item | Point to the policy language and matching-state case law (MN, IA) |

| “Overhead and profit apply only to 3+ trade jobs” | Stale 2010 rule, now “complexity and coordination” | Document the trade list: roofing, gutter, sheet metal, painting, insulation |

| ”Your appraiser is biased because he works for you” | Attacking the impartiality standard | Your appraiser is paid a flat fee, carries no contingency, has no stake in amount |

What not to do during appraisal

These are the mistakes that cost homeowners the appraisal even on a strong claim.

- Don’t name your own roofer as your appraiser. Carriers reliably challenge roofer-appraisers on impartiality, and some umpires reject them outright on that single ground. Hire an independent licensed public adjuster or retired carrier adjuster.

- Don’t run re-inspection first, then appraisal. Sequential timelines blow past most state statutes of limitation. Send both demands at the same time with withdrawal language, covered in Step 5 above.

- Don’t sign an Assignment of Benefits (AOB) contract with your roofer before appraisal. AOBs let the contractor collect directly, locking you out of scope decisions you haven’t agreed to. Florida and several other states have restricted them for this reason.

- Don’t cash any interim partial check without reading the release. Some partial checks endorse to “full and final” language that closes the claim the moment you deposit. Email the adjuster for release terms before you endorse.

- Don’t skip the policy-provision citation in your demand letter. An ADL without a cite to the exact appraisal clause gives the carrier grounds to reject it. Quote the policy section.

- Don’t argue pricing with the claim handler after demand. Once the ADL lands, every pricing conversation goes through your appraiser, not you. Claim handlers use homeowner statements against them at the panel walk.

- Don’t let the calendar slip past 9 months. Extended silence after your appraiser produced a scope is itself actionable as bad faith. Run a parallel attorney consult at month 9.

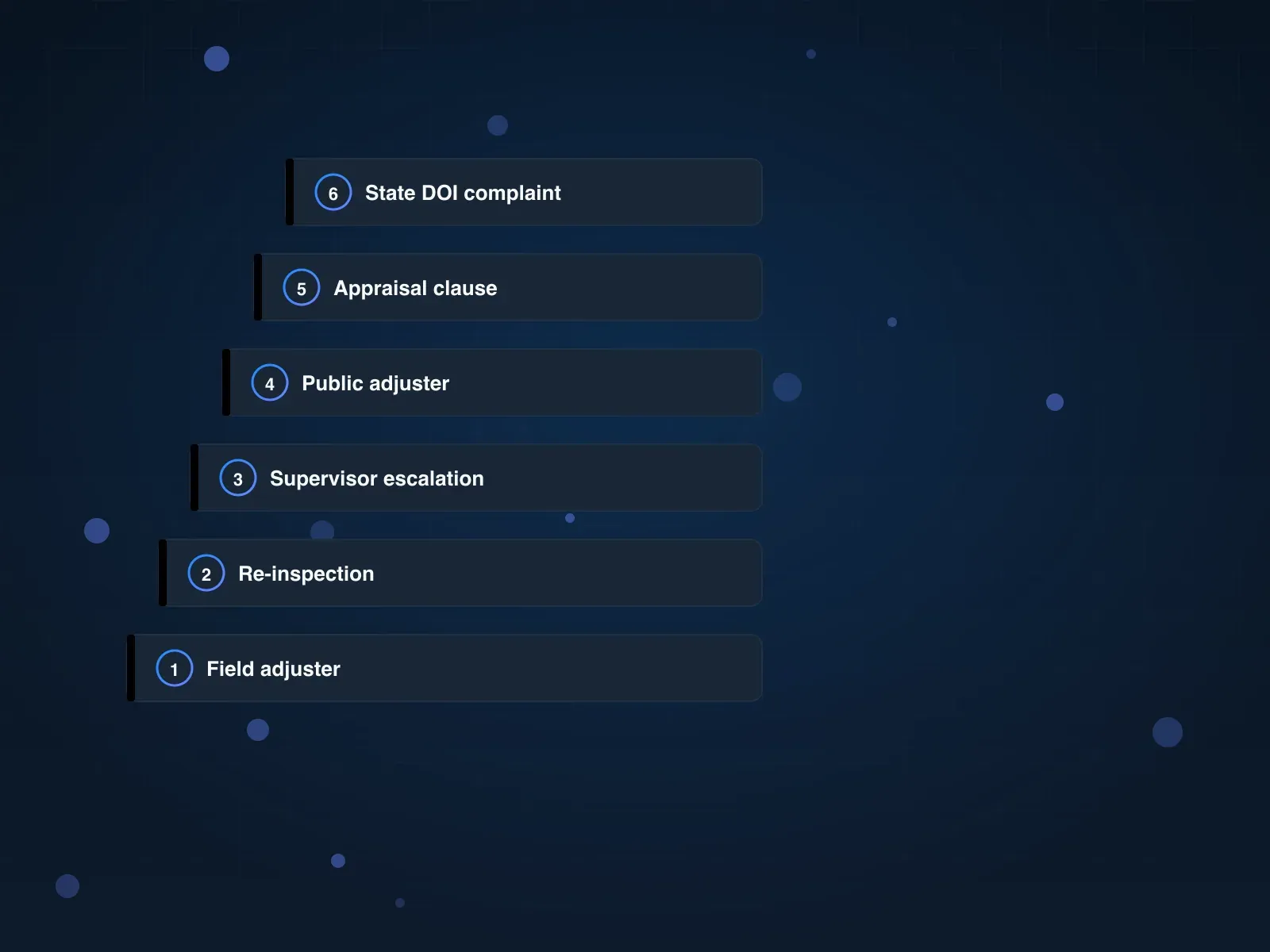

When to escalate: the decision tree

Work top to bottom. Stop at the first row that matches your situation.

| Your situation | Best next step |

|---|---|

| Carrier admits damage, you and they disagree on the dollar amount, gap over $5K | Invoke appraisal (Steps 1 to 5 above) |

| Carrier admits damage, gap under $5K | Negotiate through your roofer’s supplements; appraisal costs can eat the gain |

| Carrier denied coverage outright (“not a covered loss,” “peril excluded”) | Property-damage attorney; appraisal doesn’t apply |

| Carrier is missing statutory response windows on the ADL | DOI complaint + bad-faith attorney consult in parallel |

| Amount dispute over $75K, or multiple perils (hail + wind + water) | Public adjuster on contingency; they can run appraisal as one move |

| Carrier has not completed re-inspection yet | Send ADL + re-inspection request together; Step 5 |

| Appraisal has dragged past 9 months with no award | Bad-faith attorney; extended silence is actionable |

| Carrier accused you of misrepresentation or fraud | Attorney immediately; don’t speak to the adjuster without counsel |

Most homeowners who land in the first row resolve cleanly at the two-appraiser stage. The ones who don’t usually end up in the DOI complaint or bad-faith row within six months, because the carrier’s behavior signals it early.

Key takeaways

- Appraisal resolves amount disputes, not coverage denials. Get the denial category right before you invoke.

- PAs report settlements increasing 30% to 3,800% after appraisal on cases where the homeowner initially tried to handle the dispute alone.

- Send the Appraisal Demand Letter by certified mail and email. Carrier has 20 days in most policies to name an appraiser.

- Pick a competent and impartial appraiser. Not your roofer. $1,000 to $3,000 flat fee, plus half the umpire at $1,500 to $5,000.

- The umpire picks one appraiser’s position, not a midpoint. Any two of three panel members issue a binding award.

- Fold re-inspection into the same demand window. Do not run them sequentially; the calendar will beat you.

- Plan 3 to 6 months from ADL to check. Past 9 months, run a bad-faith attorney consult in parallel.

FAQ

How do I invoke the appraisal clause on my insurance policy?

Send a written Appraisal Demand Letter by certified mail to the claim handler and carrier’s legal department, naming your appraiser and citing the policy’s appraisal provision. The carrier names its appraiser within 20 days (most policies). The two appraisers select a neutral umpire; any two of the three issue a binding award on amount of loss.

What is an insurance appraisal demand letter?

A one-page notice that formally invokes the appraisal provision in your policy. It names your appraiser, cites the clause, and starts the carrier’s 20-day clock to name their own. Send it by certified mail with return receipt plus email for a two-dated delivery record.

How do I pick an insurance appraiser?

Hire a licensed public adjuster, a retired carrier field adjuster, a Xactimate-certified contractor with appraisal experience, or a HAAG-certified roof inspector. Do not hire your own roofer; the impartiality challenge will lose the appraisal on that ground alone. Budget $1,000 to $3,000 as a flat fee.

How does the umpire work in an insurance appraisal?

The umpire is the tie-breaker when the two appraisers cannot agree. They review each appraiser’s scope and pricing and pick one position; they do not split the difference. The award is binding when any two of the three panel members align on a number. Umpire fees run $1,500 to $5,000, typically split 50/50.

Is an insurance appraisal award binding?

Yes. The award is binding on both parties as to the amount of loss, with no appeal on the dollar figure itself. You can still pursue bad-faith claims against the carrier for delay or refusal to pay the award, but the award number does not go to court.

How much does an insurance appraisal cost?

Your appraiser runs $1,000 to $3,000 as a flat fee. Your half of the umpire runs $750 to $2,500. Total out-of-pocket for the homeowner typically lands between $1,750 and $5,500, depending on case complexity and region. Most cases recover the cost many times over at award.

How long does the insurance appraisal process take?

Plan 3 to 6 months from ADL to check. Carrier has 20 days to name its appraiser, 15 to 30 days for the two to agree on an umpire, 30 to 90 days for scoping and pricing. Award letter issues within 60 to 90 days after the scope walk. Pushy carriers stretch it to 9 or 12 months.

What is the difference between appraisal and mediation?

Appraisal is binding; mediation is not. Appraisal decides dollar amount only; mediation can address any dispute. Appraisal uses a two-appraiser plus umpire panel; mediation uses one neutral mediator. Florida and several states offer free mediation at the DOI; appraisal happens under your policy.

Can I invoke appraisal on a coverage denial?

No. Appraisal resolves amount disputes only. If the carrier denied coverage outright (peril excluded, filed past deadline, pre-existing damage, misrepresentation), appraisal is the wrong tool. You need a property-damage attorney and a DOI complaint.

Can my roofer be my appraiser?

Technically yes, but carriers reliably challenge roofer-appraisers on impartiality because the roofer has a financial interest in a higher award. Some umpires reject outright on that ground. Hire an independent licensed public adjuster, retired carrier adjuster, or Xactimate-certified third party instead.

What if the insurance company refuses to participate in appraisal?

Most state statutes require the carrier to respond to an ADL within 20 days. If they miss the deadline, file a DOI complaint citing the missed window and consult a bad-faith attorney. Courts can compel appraisal on motion; refusal to participate is itself evidence of bad faith in Florida, Texas, Colorado, Minnesota, and Washington.

Related reading

- hail damage insurance claim denial playbook (master hub)

- Allstate denied my roof claim

- State Farm roof claim denial guide

- hail under 1 inch denial dispute

- public adjuster vs attorney

- Xactimate estimate gap audit

- hail damage evidence checklist

Ready to move on appraisal? Generate a free appraisal-ready evidence pack with your NOAA hail size, roofer Xactimate summary, and the Appraisal Demand Letter template pre-filled with your claim number. 2 minutes.